-

1. Introduction

1.1 The Fundamental Contradiction of Capitalism

The root cause to the on-going economic crisis can be traced to one of capitalism's major contradictions. Labour's wage is, on the one hand, a cost of production, but, on the other hand, it is also a source of demand. This produces an inherent contradiction within the capitalist mode of production, best described in my view by Karl Marx's statement that “… the labourers as buyers of commodities are important for the market. But as sellers of their own commodity labour power capitalist society tends to keep them down to the minimum price.”1xMarx 1967a, p. 316.

Capitalism's contradictions carry the inherent possibility of crisis. Thus, zones of stability should be created to fend off such possibility. Progressive scholars believe that this can be done by means of either ‘institutional fixes’ or ‘spatio-temporal fixes’.2xJessop 2013, p. 310. The institutional fix to the aforementioned contradiction up until the 1970s was the prioritization of the wage and its treatment as a source of domestic demand. High wages in a relatively closed economy allowed the unravelling of a virtuous circle of mass production and mass consumption;3xSee Clarke 1990a, p. 71. firms were paying out high wages, which initially could be thought of as depriving them of the realization of surplus value, but since the commodity was marketed domestically with highly paid labour having an increased purchasing power as consumer, the commodity could be priced highly enough to allow firms to recoup the surplus value. This mode of development, a wage-led one, carried the name ‘Fordism’ and was a relatively stable accumulation regime.4xSee Aglietta 1976.

The gradual opening of the economies to international trade and transboundary capital movements following the oil spikes of the 1970s5xFor an account of the events leading to the transformation of the global economy starting from the 1970s, see Masouros 2013, pp. 55 et seq. has marked the advent of an era, where the aspect of wages as a cost of production came to the centre of attention by firms. In an environment where commodities increasingly came to be marketed internationally, the purchasing power of domestic labour was no longer so important. For the produced commodities to be competitive in the international arena, continuous wage repression developed in the Western economies.6xFor Europe, see Stockhammer 2007, pp. 391, 394-395, illustrating the declining wage share (= real unit labour costs in the business sector); for the US see Duménil & Lévy 2011, p. 49. This development made, on the one hand, possible the embodiment of an ever-increasing surplus value in the commodities produced but, on the other hand, was at the same time reducing the purchasing power of labour everywhere.7xMarx 1967b, p. 244. The threat emerging from this internal contradiction came to the forefront again and a fix had to be devised to ensure stability.

This fix is believed in progressive theory to have focused on the development of new forms of consumer credit and household debt.8xFor the rising trend of household debt in the United States, see Harvey 2011, p. 18; for the rising trend of household debt in Europe (although for a shorter time-period) see Stockhammer 2012, pp. 39, 55. Finance would come to complement the falling consumption power of labour.9xJessop 2013, p. 318. This new accumulation regime came to be known as the ‘finance-dominated model of development’.10xSee Boyer 2000, pp. 111-112.

In the finance-dominated accumulation regime, policy favoured the extension of easy credit to households. This, however, led to asset-price inflation and in turn to the formation of a bubble. Bubbles are destined to burst, but such bursting is not prone to cause global crises of such magnitude as the on-going one, unless other concurrent factors are in place. In this case, the deregulated shadow banking system ensured the trauma from the burst and would be widespread due to the risks from exposure to the inflated assets having been cut in slices and transferred to a large group of financial institutions.11xReference is made here to the mortgage-backed securities that transferred the risks from the burst of the housing bubble in the United States to the vast majority of investors in financial markets; for an approachable overview of the mechanisms and effects of securitization in the (shadow) banking industry see Posner 2009, pp. 41 et seq. Reference is made here of course to mortgage-backed securities and collateralized debt obligations; toxic assets allowed to flood the balance sheets of organizations worldwide due to deregulation. To be sure, deregulation was another fix of the finance-dominated accumulation regime; since finance would complement the losses from wage repression, financial institutions may well be left under-regulated.

Consequently, the ‘easy credit’ fix introduced gradually since the 1970s, did nothing more but to defer the capitalist crisis to the future, i.e. to our days. Therefore, what is said axiomatically in progressive scholarship within economic sociology, that institutional and spatio-temporal fixes may “create zones of stability here-now at the unintended cost of creating zones of instability elsewhere and/or sowing the seed of later instability”, is in the case of the on-going crisis confirmed.12xJessop 2013, p. 301.

Institutional and spatio-temporal fixes to capitalism's contradictions may create zones of stability here-now at the unintended cost of creating zones of instability elsewhere and/or sowing the seed of later instability.

1.2 Corporate Governance Configurations as Institutional or Spatio-Temporal Fixes

This article takes the view that corporate governance patterns are institutional or spatio-temporal fixes that subject to the development of complementarities with other institutions moderate the contradictions of capitalism in a given country's social order. Adopting this viewpoint upon corporate governance configurations (a viewpoint not inconsistent with the major works of the ‘politics school’ of comparative corporate governance)13xRoe 2003, p. 1, positing that corporate governance structures ensue from the ways devised by a nation to achieve and maintain social peace; Gourevitch & Shinn 2005, p. 10, positing that corporate governance patterns reflect strategic choices among players seeking to realize some kind of gains, money and security. allows us to explain a series of phenomena:

The divergent paths corporate governance has followed in different economies. Since a given social order faces a different conjuncture of contradictions, the poles, which are most problematic for the accumulation of capital, differ from country to country.14xSee Althusser 1965, pp. 204-205, who explains that a given social order experiences a principal contradiction and other secondary contradictions that in turn have primary and secondary aspects. Therefore, institutional and spatio-temporal fixes have a selective focus addressing the set of contradictions unravelling in a given economy15xJessop 2013, p. 302. and thus they are set to differ from country to country. Consequently, viewing corporate governance patterns as (the result of) institutional and spatio-temporal fixes helps explain why there are divergences in corporate governance models.

The comparative advantage a corporate governance system may provide to a country. Spatial fixes in particular carry the quality of being able to displace the contradictions of the capitalist mode of production elsewhere;16xIbid., pp. 302, 311, 315. in other words, such fixes are able to redirect, switch a crisis.17xHarvey 1982, p. 429. It is often claimed that a nation's competitiveness in the trade arena and the concomitant accumulation of trade surpluses vis-à-vis its trading partners is due to its corporate governance system (e.g. Japan's corporate governance patterns were viewed as responsible for the country's export success and for the decline of US manufacturing from 1960s onwards18xSee Lazonick 1998, p. 204.). In this respect, corporate governance patterns carry a typical characteristic of a spatial fix in the above sense, i.e. they can switch a crisis to another country.

The function of a corporate governance system as a buffer to economic shocks. Temporal fixes are a complement to institutional fixes and allow the deferral of problems into an indefinite future.19xJessop 2013, p. 311. A corporate governance model which is the result of an institutional fix of the past can, during a crisis, dictate the devise of specific fixes that shift the contradiction to the future, allowing the country having developed the model to resist in an interconnected global market the contagion of a recession.

Corporate governance patterns in a given country are institutional or spatio-temporal fixes that subject to the development of institutional complementarities moderate the contradictions of capitalism in this country's social order. As such, corporate governance configurations, particularly when they interplay beneficially with other institutions, have the capacity of redirecting a crisis to another nation (e.g. a trading partner) and/or of deferring a crisis to the future.

1.3 The Theory of Crisis and Corporate Governance: Over-Accumulation and Devaluation of Capital

To understand how important the institutions of corporate governance can prove in times of crisis (and confirm in principle theoretical propositions (b) and (c) of Section 1.2), one could resort to the Marxian theory of the crisis. The fundamental mechanism producing a crisis in this line of thought is the law of the falling rate of profits.20xManiatis 2012, pp. 6-7. There comes a point when capital accumulates at a higher rate than what can prevent the average rate of profit across the capitalist system from falling;21xHung 2008, pp. 149, 152. in simpler words, there comes a point when the capitalist mode of production produces a surplus of capital relative to opportunities to employ that capital.22xHarvey 1982, p. 192. This state of excess capital is called ‘over-accumulation’ and is the form in which pursuant to Marxian economics capitalist crises unravel. Over-accumulation manifests itself in several ways: overproduction of commodities, idle capital, surplus money capital, surplus labour power, etc.23xIbid., p. 195.

For the amount of capital in circulation to come to balance with the capacity to realize that capital through production and exchange (in simpler words, for the rate of profit to be stabilized and the over-accumulation problem to be overcome), there can be three tools:24xHarvey 1990, p. 181.

‘Devaluation of capital’,25xMarx 1973, p. 749. a process through which surplus capital is eliminated through bankruptcies, idle capital, depreciation of exchange values, and wealth inequalities, etc;

Macroeconomic control, particularly fiscal expansion, which helps absorb capital and labour surpluses in long-term projects;26xHarvey 2006, p. 96. and

Institutional or spatio-temporal fixes absorbing over-accumulation.

A society is bound to be most resilient to the devastating effects of a crisis in the capitalist mode of production, if:

it can resist the emergence of the surplus labour power form of appearance of over-accumulation (which means it will experience lower unemployment rates); and

it can deploy tools (b) and/or (c) above in response to the over-accumulation problem, rather than have to go through the devaluation route, which will necessarily lead to widespread economic misery.

In the post-2008 global financial crisis (‘Great Recession’), it seems that a Keynesian type of fiscalism [tool (b)] is largely out of the question in the West due to the sovereign debt problem and the concomitant need for fiscal consolidation going forward. Therefore, countries are bound to overcome the over-accumulation problem either through the devaluation route [tool (a)] or through institutional or spatio-temporal fixes [tool (c)]. The more a nation can rely on institutional or spatio-temporal ‘fixes’ then, the less devaluation it will experience and the less harsh its experience of the effects of the crisis will be.

Given the analysis under Section 1.2, which classified corporate governance configurations in a country as institutional or spatio-temporal fixes to the contradictions of capitalism, it follows that eventually one could posit that corporate governance does matter for the relative resilience of a country to crises, and, in our case, to the Great Recession, at least when beneficial complementarities with other institutions can be developed.

Corporate governance configurations in a country, viewed upon as institutional or spatio-temporal fixes to the contradictions of capitalism, have the potential (at least when functioning within an appropriate institutional constellation) of rendering a country more resilient to an overaccumulation crisis and to the forces of devaluation.

-

2. Varieties of Capitalism during the Great Recession: Insider v. Outsider Corporate Governance Systems and the German Case

2.1 The Effects of the Devaluation in Germany, Japan, the United Kingdom and the United States during the Great Recession

Insider systems of corporate governance are those, which in the comparative corporate governance literature are traditionally associated with bank-oriented markets, high ownership concentration of public corporations and a stakeholder orientation of management. Cross-shareholdings insulating management from hostile takeovers are common, minority shareholder protections are weak, while industrial relations are governed by a variation of cross-class coalition between labour and management (and possibly blockholders), known as ‘corporatist compromise’.27xSee Gourevitch & Shinn 2005, pp. 206-207. Insider systems of corporate governance are usually the product of the institutional nexus arising in the so-called ‘coordinated market economies’ (‘CMEs’) of the ‘Varieties of Capitalism’ (‘VoC’) approach, where firms depend more heavily on non-market relationships to coordinate their endeavours with other actors.28xHall & Soskice 2001, p. 8.

Outsider systems of corporate governance are those, which in the same strand of literature, are associated with market-oriented economies, dispersed ownership of public corporations, shareholder value orientation of management, arms-length corporate finance, strong minority shareholder protections and weak labour.29xSee Franks & Mayer 1997, p. 30; Levine 2002. Outsider systems of corporate governance are usually the product of the institutional nexus arising in the so-called ‘liberal market economies’ (‘LMEs’) of the VoC approach, where the equilibrium outcomes of firm behaviour are given by demand and supply conditions in competitive markets.30xHall & Soskice 2001, p. 8.

To be sure, the distinction between insider and outsider countries, between CMEs and LMEs, has blurred over time. The finance-dominated accumulation regime has expanded rapidly around the world over the past decades and the institutional logics of shareholder value have infiltrated even the bastions of coordinated capitalism.31xSee Masouros 2013, pp. 151 et seq. However, the process, by which such reversal in corporate governance has developed, has resulted not in displacement of the original institutions, but rather in ‘institutional layering’, where new rules are attached to existing ones thereby changing the way in which the original rules structure behaviour.32xMahoney & Thelen 2010, p. 16. Therefore, at least the remnants of the original institutions are there and can make a difference in the path firms follow even under a globally converging model of capitalism.

If corporate governance patterns in a given country can, through their interplay with other institutions (e.g. industrial relations, monetary policy, etc.), operate as institutional or spatio-temporal fixes to the contradictions of capitalism, then given such fixes’ function as crisis-switchers and/or crisis-buffers, we should expect to note differences between insider and outsider countries in their performance during the Great Recession.

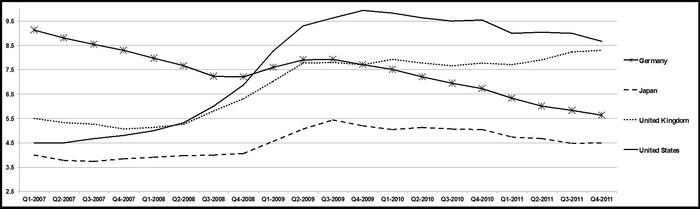

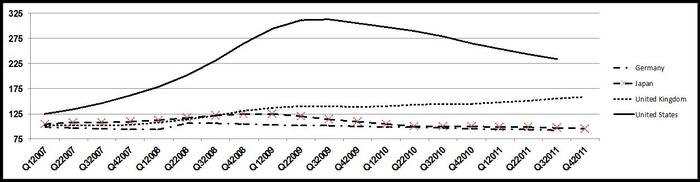

To test whether such differences exist, we should seek data on the degree of devaluation insider and outsider countries have undergone during the Great Recession. Proxies for the degree of devaluation a country goes through during a crisis are the developments in the unemployment rate, the number of bankruptcies33xClarke 1990, pp. 442, 446. and wealth inequality; comparing data on these variables for the period of the Great Recession in representative countries of the insider and outsider systems of corporate governance can provide an indication as to the quality of each system's patterns as institutional or spatio-temporal fixes. Figures 1 and 2 below feature a comparison of the unemployment rate and the number of bankruptcies, respectively, in the United States and the United Kingdom on the one hand (representative countries of the outsider model of corporate governance) and Germany and Japan on the other hand (representative countries of the insider model of corporate governance) for the time period 2007-2011; Figure 3 features a comparison of the changes in the Gini coefficient (measure of inequality) between the same countries for the time period 2007-2010.34xCoverage of the post-2012 period was left out due to the abundance of factors affecting the economies of the sample after 2011 that would not allow to confirm the linkage between corporate governance and response to the Great Recession (e.g. the Great East Japan Earthquake of 2011, “Operation Twist” initiated by the Fed in the United States in late 2011, the “domino” effect of the periphery's crisis within the Eurozone, etc.).Unemployment rate 2007-2011 Source: OECD Statistics. Number of bankruptcies 2007-2011

Source: OECD Statistics. Number of bankruptcies 2007-2011 Index 2006 = 100.

Index 2006 = 100.

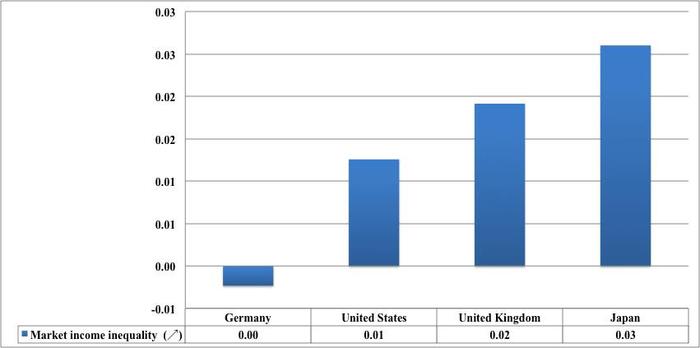

Source: OECD, “Recent Trends in New Firm Creations and Bankruptcies”, in Entrepreneurship at a Glance, OECD 2012.Percentage point changes in the Gini coefficient of household market incomes between 2007 and 2010 Source: OECD, Crisis Squeezes Income and Puts Pressure on Inequality and Poverty New Results from the OECD Income Distribution Database, OECD 2013.

Source: OECD, Crisis Squeezes Income and Puts Pressure on Inequality and Poverty New Results from the OECD Income Distribution Database, OECD 2013. As far as the development in the unemployment rate following the advent of the Global Recession (Figure 1) is concerned, it is observed that although Germany enters the crisis with a higher unemployment rate than the United States and the United Kingdom, it manages to gradually drive such rate down at the same time that the two countries of the outsider model mark an exponential increase in the unemployment levels. Japan enters the crisis with a lower unemployment rate than all countries of the sample, but experiences proportionally only a minimal increase in such rate compared with the outsider countries.

As far as the development in the number of bankruptcies (Figure 2) is concerned, it is observed that despite a modest increase in such number in the ‘insider’ countries following the advent of the Global Recession, the number of bankruptcies in these two countries stabilizes at pre-crisis levels (or even lower) from Q2 2009 onwards, at the same time that the ‘outsider’ countries experience an exponential increase in the number of bankruptcies.

The prima facie outcome of the comparison in Figures 1 and 2 is that the representative insider countries are resisting the forces of devaluation more effectively compared with the representative outsider countries. However, Figure 3 challenges this initial conclusion by indicating that, while wealth distribution in Germany remained unchanged, the other insider country, Japan, championed the rise in inequality. This discrepancy in the results does not allow one to declare an undisputable winner in the ‘battle of the systems’; it allows, however, to declare a single variety of capitalism within the CMEs, the German one, as a winner.

The countries of the insider model of corporate governance (CMEs) show overall a greater resilience to the effects of the crisis-associated devaluation, since compared with the countries of the outsider model of corporate governance (LMEs) have a lower rise in unemployment rates and a more modest rise in the number of bankruptcies during the Great Recession. However, Japan (an insider country) shows a greater increase in income inequality during the Great Recession than the outsider countries and thus Germany emerges as a unique case of resilience to the crisis.

2.2 The Shareholder Value-Driven Rise in Income Inequality in Japan

Japan's variety of capitalism was traditionally considered similar to Germany's; the two countries were examples of ‘welfare capitalism’ in juxtaposition to Anglo-American ‘stock market capitalism’.35xSee Dore 2000. The Japanese ‘companyist’ accumulation regime has undergone, however, significant change through the reforms towards shareholder value.36xSee Isogal 2013, p. 31.

The ‘companyist’ mode of régulation in Japan developed in the post-War period around the preference of workers for job security and lifetime employment.37xSee Gourevitch & Shinn 2005, p. 169. Complementary institutions were developed in Japanese corporate governance that would ensure such security. Employment security required management security, i.e. insulation from hostile takeovers and proxy fights, and the ability of management to adopt long-term horizons.38xYamada & Hirano 2013, pp. 20-21.

Management security required a stable shareholder base. Since the Allied Occupation expropriated the old blockholders, ownership of Japanese corporations remained dispersed. Thus, synthetic blockholders were created through the keiretsu, a dense network of cross-shareholdings between affiliate firms that insulated management from being voted out and/or from hostile takeovers. Liberated from market pressures corporate management in Japan developed a system where managers were promoted from within, thus providing a long-term incentive to employees to develop firm-specific skills.

Long-term corporate horizons were secured through a bank-oriented corporate finance market. In the paradigm picture of Japanese corporate governance, there is a ‘main bank’, which acts as significant shareholder and as principal creditor to the firm. It monitors the business affairs of the company closely, providing leeway to management in the normal course of events, but acquires a key role in times of financial distress by undertaking rescue operations.39xAoki 1990, pp. 1, 14-16.

To the extent that there are remnants of the keiretsu and ‘main bank’ institutions in Japanese corporate governance, this could help explain both the low unemployment rate and the low number of bankruptcies in Japan during the Great Recession (Figures 1 and 2). On the one hand, close monitoring by the ‘main bank’ ensures an early detection system for problems40xIbid., p. 15. that may avert the firm from entering the zone of insolvency, while rescue operations (incl. emergency financing and loan restructuring) prevent the filing of a bankruptcy petition.41xOn the relationship between the risk of bankruptcy and the ‘main bank’ system, see Hoshi & Scharfstein 1990, p. 67. On the other hand, the insulation of management from profitability pressures associated with equity financing allows the firm to take a long-term view and defer the timing of downsizing that could lead to lay-offs in times of financial distress,42xSee Noda 2013, p. 363. while the keiretsu structure allows for work sharing arrangements between the keiretsu affiliates, so that surplus labour in one firm of the network can be absorbed by another firm in the cross-shareholding network.

As it has happened with other representatives of the insider model of corporate governance (e.g. Germany), these features of Japanese corporate governance have lately underwent pressure. Banks have been forced to disinvest from equity positions in corporations in order to comply with the Basel Accords43xYamada & Hirano 2013, p. 18. and foreign owners looking for (short-term) returns on investment have taken their place.44xSee Ahmadjian 2007, p. 125. Overall, deregulation in corporate finance brought about a shift towards raising funds from capital markets.45xYamada & Hirano 2013, p. 18; see Hoshi & Kashyap 2004. Following the decline of bank dependency, the keiretsu system declined as well; studies have shown that cross-shareholdings of firms listed in the Tokyo Stock Exchange have dropped from an average of 18% in a firm's shareholder structure in 1990 to less than 8% in 2003.46xSee Kuroki 2003.

Given that the system of bank and keiretsu guaranteed management security, which functioned as an institutional complement to employment security, declined, Japanese labour relations underwent transformations as well. First of all, shareholder value-oriented foreign shareholders have been found to be associated with increased downsizing among firms;47xSee Ahmadjian & Robbins 2005, p. 451. on average, it seems that while Japanese firms were in a position to maintain employment intact until after having realized losses for two consecutive years, they now, under the influence of foreign owners, begin downsizing after the first year of losses.48xNoda 2013, p. 363. Furthermore, labour-management practices oriented towards lifetime employment have changed amidst a trend of an increasing non-regularization of workers that results in part-time, fixed-term, dispatched, etc. employment for a lower wage than the one associated with permanent core employment.49xYamada & Hirano 2013, pp. 20-21. Today, two thirds of the labour force in Japan are regular workers, while one third are non-regulars,50xIbid., p. 21. which is a clear sign of dualism in the Japanese labour market that carries an explanatory force for the increasing market income inequality observed in Japan (Figure 3).2.3 Germany's Road to Financialization

The institutional layering in Japan has led to a hybridization of the Japanese firm, which blends traits of the shareholderist and the stakeholderist system. To be sure, Germany has also witnessed this hybridization as German corporate governance has come under pressure from a financialized environment. The German system of corporate ownership is transforming as holdings by large shareholders have been replaced by stakes held by (foreign) institutional investors; banks, which traditionally have been influential even in equity governance within German firms, have also reduced their exposure to equity positions.51xVitols 2004, pp. 357, 365-367. Bank credit's significance for corporate finance has also reduced over the years,52xVan Treeck et al. 2007. thus removing to some extent from German corporate governance the element of long-term patient capital.

German industrial and labour relations have also undergone transformation leading as in the case of Japan to an increasing dualism in the labour market. When in the early 1990s German firms were challenged by (a) increased product market competition (particularly from East Asia and Japan) arising from the globalized markets, (b) Germany's reunification, which had led to a pay hike, (c) an overvalued exchange rate in the European Monetary System and (d) the 1992/1993 recession, they launched a process of ‘cooperative modernization’ (Prozess kooperativer Modernisierung).53xKommission Mitbestimmung 1998, p. 13. This process involved ‘company- or plant-level employment pacts’, by which employers would bargain with the workforce on the micro-level (i.e. outside industry-wide collective bargaining) in order to cut labour costs and increase productivity in exchange for withdrawal of announced lay-offs, no-redundancy clauses, employment guarantees and future investments in the plant.54xJackson, Höpner & Kurdelbusch 2005, p. 91; Zagelmeyer 2001, pp. 149, 152. By means of the pacts employees avoided a relocation of the plants to more cost-competitive jurisdictions and stabilized core employment, while employers managed to moderate wage increases, avoid strict overtime rules, secure a more flexible working time and transfer service (non-core) components of the plant (e.g. canteen, security) to other collective agreements and lower pay.55xData show that already during the 1990s almost half of the largest firms in Germany (55 out of 120) negotiated a company-level pact and that within these 55 companies at least 156 agreements can be found; see Hassel 2014, p. 66. This shift of collective bargaining to the company or plant level was made possible through derogation clauses in the industry-wide collective agreements.56xSee Haipeter 2011, p. 679.

It seems, therefore, that the path followed in Germany is not different than the one followed in Japan. Still it seems that the infiltration of the institutional logics of shareholder value has damaged Japan more than it has damaged Germany. The question is, then, what is the reason why the German corporate governance configurations seem to have been more potent as institutional or spatio-temporal fixes despite the two countries' parallel paths towards financialization and shareholder value?2.4 Germany versus Japan: Does the Key to Germany's Resilience Lies within an EMU-Driven Institutional Complementarity?

Corporate governance configurations do not function in a vacuum. They interact with other institutions, and this interaction can drive economic activity to sustainable competitiveness or failure. Within a production regime, the functionality of an institutional form is conditioned by other institutions; complementarities between institutions arise.57xHöpner 2005, p. 331. It follows that the potency of corporate governance configurations as institutional or spatio-temporal fixes to the contradictions of capitalism cannot be examined in isolation, as it is also dependent on such configurations' interplay with other institutions within a said production regime. This is the concept of ‘institutional complementarity’. Part of the explanation why Germany has resisted all forces of devaluation as opposed to its institutional relative, Japan, could be the emergence during the recent years of some new institutional complementarity within the German variation of capitalism.

There have been two structural regional developments affecting Germany and Japan since the time that the two countries were being identified as bastions of ‘welfare capitalism’. Differences in the interaction of the two countries' corporate governance and industrial relations institutions with these developments might carry an explanatory force for the different level of resilience these two economies are showing to the Great Recession. For Germany, the major transformation is the development of the European Monetary Union (‘EMU’), while for Japan it is the exponential growth of trade flows into, out of and within the East Asia region. Given the two countries’ export dependency, it seems logical to test how their ‘trade reflex’ to these separate developments has been.

Germany's export performance seems to have benefited from the development of the EMU. Between 1994 and 2009, Germany devalued its real unit labour costs in relation to its European competitors by 20%.58xSee Marin July 2010. The increase in the value of German intra-EU dispatches between 2003 and 2010 was 32.4%, while during the same period Germany maintained intact its market share in intra-EU dispatches at 22.5%, at the same time that France's market share dropped from 12.5% in 2003 to 9.5% in 2010 and Italy's from 8.6% to 7.6%.59xEurostat, External and Intra-EU Trade. A Statistical Yearbook, Data 1958-2010, Eurostat Statistical Books, p. 84. Germany accumulated a trade surplus vis-à-vis its European partners that increased by 62% between 2003 and 2007, the year before the Great Recession started.60xIbid., p. 82. Germany's increase in the value of extra-EU exports marked an increase of 62.3% with its market share (compared with other EU Member States) increasing from 26.8% in 2003 to 28.1% in 2010, at the same time that France's market share dropped from 13.3% to 11.4% and Italy's from 11.5% to 10.7%.61xIbid., p. 86.

While Germany was accumulating trade surpluses vis-à-vis its European partners and was effectively rendering the latter less competitive in the international trade arena, Japan was not increasing its market share in intraregional trade in the East Asian region despite such trade's exponential overall increase during the past two decades.62xSee International Monetary Fund 2011, Figure 6.1, p. 33. Data show that since the mid-1990s newly industrialized economies, such as Indonesia, Thailand, Malaysia and the Philippines, increasingly account for a larger part of the intraregional trade, as opposed to Japan. In addition to this, while an export similarity index in 1995 would show that Japan is competing mainly with advanced Western economies, in 2008 it would show that competition by regional trading partners, such as China and Thailand, is also increasing.63xIbid., p. 27.

The competitiveness issues Japan is increasingly facing in East Asia seem to be the result of the choice of Japanese firms to offshore parts of the production chain in other low labour cost countries of the region. As part of what is known as ‘Factory Asia’, Japanese firms in high-technology sectors have transferred production sites to other countries in the region. While research and development still takes place in the headquarters, trade flows have shifted from Japan to other Asian countries.64xIbid., p. 23. The increasing availability of low labour cost production locations for Japanese firms in the region created downward pressure on employment protection and wages for less skilled labour within Japan with the result being the dualization of the Japanese labour market and the apparent increase in income inequality.

The above comparison shows clearly that despite their institutional similarities, Germany has emerged from its own regional transformation stronger, while Japan's position has become weaker. The reason is that the development of the European Exchange Rate Mechanism (‘ERM’) and the EMU created a new institutional complementarity between German corporate governance, German industrial relations and the institutions of the currency union that produced a beneficial outcome. Institutions do not exert influence on political economy equilibriums one at a time, but jointly. This new institutional complementarity allowed Germany to deepen its export-led growth strategy, outperform the EU Member States in terms of competitiveness and eventually acquire resilience to the Great Recession by emerging as a ‘safe haven’ within a crisis-struck Europe.

The European Exchange Rate Mechanism and the European Monetary Union gave rise to a new institutional complementarity between German corporate governance, German industrial relations and monetary institutions that provided a boost to Germany's competitiveness. This competitiveness increased Germany's resilience to the Great Recession compared with other coordinated market economies, such as Japan, and allowed it to capitalize on the overall more crisis-resilient features of the insider model of corporate governance.

-

3. The Institutional Complementarity between German Corporate Governance, Industrial Relations and the European Monetary Union

There are three poles in the institutional complementarity we seek to point to in this article for the German case: monetary institutions (including institutions of the European Exchange Rate Mechanism and the EMU), industrial relations and corporate governance. Sections 3.1 and 3.2 below discuss monetary institutions and industrial relations, while Section 3.3 discusses corporate governance.

3.1 The Interaction between Central Bank Independence and Coordinated Collective Bargaining and the European Exchange Rate Mechanism

The key to the resilience of the German economy during the Great Recession is its competitive positioning among the EU Member States as an exporter. This competitive positioning was already present since the days of the European Exchange Rate Mechanism (‘ERM’), which was the predecessor to the EMU. By taking advantage of the beneficial interaction between the institutions of the ERM, the German industrial relations system and corporate governance configurations, Germany entered the EMU era by having already augmented its comparative advantage vis-à-vis its European partners. The ERM-spurred increased competitiveness of Germany then deepened the structural asymmetry of the EMU, which as it is shown below (Section 3.2) is bound to transmit crises from the surplus to the deficit countries within the currency union.

It is well documented in scholarship that the independence of a central bank allows for non-inflationary wage setting where wage bargaining is more coordinated.65xSee Hall & Franzese 1992, p. 505. Mainstream theory suggests that uncertainty about the future direction of monetary policy results in trade unions seeking an ‘inflation increment’ on wages;66xIbid., p. 507. as a result, labour unit costs will go up and competitiveness will be eroded. It is, therefore, posited that the independence of a central bank of political control increases its credibility regarding assurances that monetary policy will remain tight and thus allows wage bargainers to lower the nominal wages they bargain for.67xSee Rogoff 1985, p. 1169. Thus, in mainstream theory, independent central banking is associated with trade competitiveness.

However, in a challenge to the mainstream theory it has been documented that the central bank's independence cannot have the effect described above unless wage bargainers can coordinate their behaviour. When there are many wage bargainers within an economy, then even if one set of bargainers is willing to perceive the signal of the central bank as credible, it cannot know how another set of bargainers will react to such signal. In the presence of uncertainty regarding other bargainers’ behaviour, the wage-setters are likely to seek an ‘inflation increment’ despite central bank's independence;68xHall & Franzese 1992, p. 508. they price in the wage settlement the eventuality that other bargaining units will attain a more favourable wage settlement. Therefore, even in the presence of central bank independence, uncoordinated wage bargaining can erode trade competitiveness.

Collective bargaining in Germany was and still is able to fend off against the uncertainty caused by multiple-level wage bargainers' behaviour because it possesses a pair of bargainers in a leading sector with sufficient economy-wide linkages that allow it to transmit its settlement across the economy.69xIbid., p. 510. The powerful metalworkers union, IG Metall, that represents workers in a range of export-oriented industries (incl. automobiles, engineering and steel) is considered a lead bargaining unit, and its wage settlement with the corresponding employers' federation, Gesamtmetall, is considered a pacesetter in German collective bargaining.70xRaess 2013, pp. 1, 5. Because of IG Metall's leverage, other unions in Germany know that it is unlikely that they will succeed a better wage settlement than IG Metall. Thus, other wage bargainers are inclined to follow its lead. IG Metall, knowing that its wage settlement is likely to be generalized, need not build in an inflation increment, and thus the wage setting does not increase labour unit costs in an uncontrolled manner.

An independent central bank is likely to respond directly to the wage settlement of the lead bargaining unit because such settlement will have economy-wide effects. The lead wage bargainers are aware of the fact that the central bank has focused its attention to their bargaining round, and therefore they are unlikely to struck a wage settlement that might be perceived by the central bank as inflationary and thus trigger an extra-tightening policy that might dampen the economy. In the German case, such interaction is illustrated by the statements and counterstatements exchanged between IG Metall and the Bundesbank during bargaining rounds.71xSee Streeck 1994, pp. 118 et seq. To the contrary, in an uncoordinated wage-bargaining setting, bargaining units have no reason to expect a direct response to their settlement by the central bank even an independent one and thus they do not have an incentive to exercise moderation.

It follows that, unlike other Member States with less coordinated wage-bargaining environments, Germany was, before the replacement of the Bundesbank by the European Central Bank, able to secure wage restraint and thus an increased level of trade competitiveness. As it was mentioned above, the comparative advantage that this institutional interaction endowed Germany with was particularly pronounced during the days of the ERM. This is because, in essence, during this period, the Bundesbank was acting as the ERM's real central bank;72xThere is widespread agreement in literature that the ERM was functioning as a D-mark zone. The Bundesbank was choosing its money supply independently and provided a nominal anchor for the system, as other member countries were devoting monetary policy to keeping the DM exchange rate fixed; see McKinnon 1993, p. 1; Russo & Tullio 1998; Giavazzi & Giovannini 1989; Herz & Röger 1992, p. 1413. thus, German collective bargaining could continue to produce the moderate results that Germany's export growth strategy required, but at the same time uncoordinated collective bargaining in other Member States that were parties to the ERM was set to produce increased inflation and erode their own competitiveness. This asymmetric effect of the ERM on collective bargaining in Germany and the other ERM members has been clearly stylized in theory indicating the competitiveness gain that Germany was extracting through wage moderation domestically and wage inflation abroad.73xSoskice & Iversen 1998, pp. 110, 116-117.

Consequently, so far we see the institutional complementarity between German industrial relations (more precisely collective bargaining) and the institutions of the ERM that produced a beneficial outcome for Germany's performance in the years immediately preceding the introduction of the EMU.

Central bank independence promotes price stability and wage moderation only when collective bargaining is coordinated. German collective bargaining is coordinated and leads to wage moderation because of the interaction between the Bundesbank and the metalworkers' union, IG Metall, that is a pace-setter for bargaining in other industries. During the days of the ERM, the Bundesbank was the only real central bank in the union and German labour costs were thus set to remain low, at the same time when uncoordinated collective bargaining in other Member States was set to produce inflationary wage setting.

3.2 The Political Economy of Cash Flows within the (Asymmetrical) EMU

Once Germany was inside the EMU with the ERM-spurred augmented comparative advantage vis-à-vis its European partners, such advantage was bound to deepen further and in particular to endow German institutions with a crisis-switching ability. The obvious explanation for this would be that the Member States of the EMU entered a situation where national currencies' manipulation as an adjustment tool for competitiveness had ceased to exist and the state of ‘competitive corporatism’ had emerged, in which wage moderation was instrumental for maintaining real exchange rate competitiveness.74xGalanis 2013, pp. 475, 489. However, the beneficial outcome of the institutional complementarity between German corporate governance, industrial relations and the EMU was preserved not only because of the undisputed ability of the German institutions to win the ‘competitive corporatism’ race, but also because of the political economy of cash flows within a structurally asymmetrical currency union, such as the EMU.

Within a monetary union, a surplus nation, such as Germany, has the propensity to recycle its surpluses through capital flows to the deficit nations of such union.75xVaroufakis 2013, pp. 51-52. Profits from exports turn into savings in the surplus nation, since profits accumulate at a higher rate than the investment required in production units; the glut of savings pushes interest rates downwards and rates of return are reduced in the surplus nation. The funds seek a higher rate of return, so they are channelled to the deficit nations. At the same time these capital outflows finance the trade deficit of the nations of the monetary union and thus the surplus nation indirectly supports demand for its exports.76xHalevi & Lucarelli 2002, pp. 24, 26.

Effective demand in the deficit nations receiving the capital inflows increases and becomes a driver of rapid economic growth, but when the union is asymmetrical, in the sense that deficit nations do not possess the institutions that will allow them to turn the funds into productivity-enhancing activities, then the inflows result in asset value inflation in the deficit nations and GDP growth rates that exceed fixed capital formation.77xVaroufakis 2013, p. 53. This is the perfect recipe for a bubble economy. At the same time, surplus nations by: (a) having reached a maturity stage (the industrial sector has up-to-date capital stock and the needs can be met with little new net investment78xHalevi & Lucarelli 2002, p. 30.); (b) curbing domestic demand through a price stability-driven monetary policy and a repressive wage policy; and (c) keeping asset prices low because of the capital outflows, experience a slower growth rate than the deficit nations. Paradoxical as it may seem on first sight, this slow growth rate in the surplus nations of a monetary union is exactly what carries within it the sperm of a future crisis in the deficit nations.

The data collected on the economic trends within the EMU until the Great Recession struck reveal a divergence between surplus and deficit nations of the kind described exactly above. For the years 1999-2006, Germany saw its GDP growing on average 1.3% per year, while the countries of the periphery of the EMU were growing much more rapidly: Greece experienced a 4.3% annual growth rate, Ireland a 5.9% one and Spain 3.6%. At the same time, while the cumulated change of domestic demand in Germany was 2.5%, in Greece it was 33.9%, in Ireland 48.2% and in Spain 34.7%. The periphery nations of the EMU were developing an economy reliant on consumption, while Germany was deepening its export-led growth strategy. Germany's net exports during the same period were increasing at 4.2% p.a., while Greece's net exports at only 0.8% p.a., Ireland's net exports were decreasing at 2.8% p.a. and Spain's decreasing at 4.4% p.a.79xData retrieved from Priewe 2007, p. 113. The periphery countries had lost their price competitiveness to Germany and with it the export race.

Germany's slow growth rates in combination with its substantial budget deficit before the Great Recession created a path destined to bring the debt-to-GDP ratio in the long-term to unsustainable proportions. The pressure to eventually keep in line with the Stability and Growth Pact standards80xArticle 126(2) TFEU; Protocol on the Excessive Deficit Procedure, Article 1. mounted through a number of reforms at the EU level in 2005,81xRegulation 1055/2005/EC amending Regulation 1466/97/EC on the strengthening of budgetary positions and the surveillance and coordination of economic policies, OJ 2005 L 174/1; and Regulation 1056/2005/EC amending Regulation 1467/97/EC on speeding up and clarifying the implementation of the excessive deficit procedure, OJ 1997 L 174/5. and thus Germany would have to reverse the capital flows: a ‘sudden stop’.82xSee Sinn & Wollmershäser 2012.

The timing of such EMU-driven reversal of capital flows largely coincided with the advent of the Great Recession that squeezed the asset bubbles in the periphery to burst faster than expected. In a monetary union, the deficit nations can no longer correct the trade imbalance by currency depreciation, and thus they are forced to an internal devaluation in hope that wage and price reductions will stimulate domestic production. This causes defaults on bank loans, the State is forced to intervene and transfer private debts to the public purse and the end result is recession in the deficit nation. This is exactly what happened to the deficit nations of the EMU periphery during the Great Recession.

Having lost also their price competitiveness to Germany, financial markets presumed that these deficit countries could no longer follow an economic growth path and thus an investors' flight to safety to the surplus nation, Germany, ensued. Thus, on the one hand Germany stopped the recycling of export profits to the periphery and on the other hand with its undisputable competitiveness managed to siphon the majority of fresh funds directed to the EU. The German institutional complementarity between the EMU, corporate governance and industrial relations gave rise to a synthetic spatio-temporal fix that switched the effects of the Great Recession to other nations within the EMU and particularly to those of the periphery.

Germany entered the EMU as a surplus nation and within a monetary union a surplus nation has the propensity to recycle its surpluses through capital flows to the deficit nations of such union. Demand in the deficit nations receiving the capital inflows increases, but when the union is asymmetrical (see EMU), in the sense that deficit nations do not possess the institutions that will allow them to turn the funds into productivity-enhancing activities, then the inflows result in bubbles. Surplus nations experience slow growth rates because of the capital recycles and at some point they have to reverse capital flows; this, leads to a ‘sudden stop’ in deficit nations and the bubbles burst. Thereafter, investors begin a flight to safety to the surplus nation that deepens the crisis in the deficit nations. Thus, the surplus nation's trade competitiveness results in the switching of a crisis to the deficit nation. This is exactly what happened with Germany (surplus nation) and the Eurozone periphery (deficit nations) during the Great Recession.

3.3 The Role of German Corporate Governance in the New Institutional Complementarity

So far, we have examined the institutional domains of the ERM and the EMU and elements from the domain of German industrial relations. To complete the examination of this unique institutional complementarity that endowed Germany with its competitiveness within the EMU and further with its resilience to the Great Recession, this sub-section reviews the contribution of corporate governance to the institutional interaction.

As mentioned under Section 2.4 above, between 1994 and 2009 Germany devalued its real unit labour costs in relation to its European competitors by 20%. From 2000 to 2010, the annual average growth in Germany's labour costs (per hour worked in the private sector) was 1.7%, while during the same period labour costs increased by 2.8% p.a. in the EMU and by 3.3% in the EU27.83xT. Niechoj et al., December 2011, pp. 2-3. To be sure, the same trend holds true for the average annual growth rate of labour costs in the manufacturing sector, which is the backbone of Germany's export industry.84xIbid., p. 8. This massive moderation of labour costs was initiated by the process of ‘cooperative modernization’ that sprung within German corporations following the challenges of the early 1990s (see above Section 2.3).85xThere is, however, a strong position in scholarship that Germany's competitiveness is owed to the off-shoring of parts of the production chain to Eastern Europe, where there is skilled low-cost labour; see Marin, 20 June 2010, VoxEU.org. The cross-class consensual environment that German corporate governance had already nurtured and the long-term incentives that German corporate finance was providing to bargaining parties were instrumental to the transformation and functioning of the German system of industrial relations, which through its interaction with the monetary institutions of the ERM and the EMU endowed Germany with the comparative advantage discussed under Section 2.4 above.3.3.1 The Codetermination-Driven Success of the Decentralization of German Collective Bargaining

German industrial relations became increasingly dualized during the 1990s, a development that endowed the German export sector with the necessary flexibility in order to champion an increasingly competitive global trade arena. On the one hand, the German system of industrial relations continued to rely on industry-wide collective bargaining with IG Metall being the pace-setter in order to ensure monetary stability (see Section 3.1), but on the other hand it moved towards decentralization by delegating a good deal of authority to the company and/or plant level. As mentioned above (see Section 2.3), this decentralization involved company- and/or plant-level employment pacts, by which employers would bargain with the workforce in order to cut labour costs and increase productivity in exchange for withdrawal of announced lay-offs, no-redundancy clauses, employment guarantees and future investments in the plant. Works councils, as defined in the German Works Constitution Act of 1952, were instrumental in accommodating the shifting of bargaining responsibility to the company and/or plant level.

Although these employment pacts were not the result of legal institutions that fall strictly within the field of corporate governance, but were rather the result of labour law processes (e.g. derogation clauses in industry-wide collective agreements, particularly following the so-called ‘Pforzheim Agreement’ of the metalworking industry in 200486xSee Bispinck 2005, p. 301.), it is acknowledged that the institutions of German corporate governance played a pivotal role in the pacts’ success.87xStreeck, December 2001, 3.1.4. German corporate law requires half of the seats of the supervisory board of corporations that employ more than 2,000 persons to be occupied by employee representatives. Complementary to the provision on codetermination at the supervisory board level is the aforementioned law on works councils, which endows the latter with certain codetermination powers at the plant level as far as working conditions are concerned. These legal provisions provided both labour and management with an underlying assurance against possible opportunism of the other side and thus created a trust and good faith environment for concession bargaining at the company and/or plant level.88xKommission Mitbestimmung 1998, p. 76. This is consistent with the general argument of ‘actor-centric institutionalism’ that posits that institutions are truly embedded only when sustained by a balance of power and/or balance of trust.89xGumbrell-McCormick & Hyman 2006, pp. 473, 490. In other words, there is an apparent complementarity between the bargaining institutions at the company and/or plant level and the stakeholder institutions of German corporate governance, particularly the one of employee representation at the supervisory board level. The fact that the scope for bargaining on employment becomes greater when a legal infrastructure promoting co-decision making is already in place is confirmed by the poor when compared with Germany results of concession bargaining in other European plants during the ‘European Car Wars’ of the 1990s.90xSee Zagelmeyer 2001, p. 167. This corporate governance-driven ‘embedded collectivism’ of the German stakeholders ensured that the decentralization of collective bargaining would be experienced as a beneficial development in German industrial relations.3.3.2 Negotiated Shareholder Value

The moderation of labour costs in the German industry occurred in an environment where shareholder value was exerting an influence to corporate decision making, albeit not a decisive one that could have led to US-style downsizings. This corporate governance environment that has come to be known as one of ‘negotiated shareholder value’ was instrumental, particularly during the Great Recession, when German firms engaged in labour hoarding91xHassel 2014, p. 75. resulting in the low unemployment rates observed in Figure 1.

The experience of German firms with employment pacts at the company- and/or plant-level proved valuable, particularly for the manufacturing sector, as in the post-2008 era the pacts were used once again as an adjustment mechanism to reduce working hours, introduce job rotation and extra holidays.92xIbid., pp. 75-76. Despite German corporate law's increasing orientation towards shareholder value,93xSee Masouros 2013, pp. 216-217. Germany's stakeholder configurations acted as constraints to the forces that could have dictated ‘outsider-like’ strategic choices to actors leading to redundancies. The impact of shareholder value-enhancing reforms was mediated by the relevant rules' interaction with the strong position that employees have in German corporate governance; short-term strategies of shareholder value which in countries of the outside system of corporate governance can be adopted unilaterally thus remained contingent upon a negotiated process between labour and management that subjected the corporate governance of German firms to a more long-term horizon.94xGoyer 2012, pp. 161, 163. This corporate governance state, in the framework of which shareholder interests cannot be transformed into business decisions through the traditional management channel but have to be negotiated first with other members of the stakeholder coalition, is known as ‘negotiated shareholder value’ and is a distinctive trait of German corporate governance,95xSee Vitols 2004, p. 51. which allowed German firms to retain their employees through concessions that did not give rise to a conflictual situation.3.3.3 Insulation from Hostile Takeovers and Capital Market Pressures

The German legal infrastructure ensuring protection from hostile takeovers also contributed to the level of trust required for cooperative industrial relations, since in the eyes of the workforce it ensured the relevant continuity of the incumbent management, which was necessary for the credibility of future promises as to investments. Beyond this logical observation, the fact that weak and less influential financial markets are complementary to cooperative relations between labour and management has been stylized in scholarship.96xSee Amable, Ernst & Palombarini 2005, p. 311. When capital markets pressurize corporations for reversibility and flexibility, then collective bargaining favours short-term strategies for each side and lack of involvement in the employment relationship. Patient capital, however, signals to social partners that they may devise long-term arrangements, and this facilitates cooperation in bargaining.97xIbid., pp. 316-317.

To be sure, the model that stylizes the complementarity between corporate finance and industrial relations advocates that the institutional form that corporate finance takes in a given economy in fact dictates what institutional form of industrial relations should take in order to increase the firm's survival probability. When financial markets’ pressure is low, then labour and management choose long-term strategies, and this further promotes cooperative collective bargaining. When financial markets pressure is high, labour and management choose short-termist strategies and cooperative bargaining is undermined. Insulation from capital market pressures and cooperative bargaining are in other words a stable institutional combination.98xIbid.

The insulation from capital market pressures is attained at a sufficient albeit not decisive degree, when the threat of hostile take-overs is low. An active market for corporate control and the non-ability of managers to protect their firm from it is in paradigm agency theory thought of as one of the greatest disciplining forces for management, which has to devise strategies to keep the share price high at all times. In legal orders where management has the ability to adopt take-over defences, the pressure from equity markets is to a great extent reduced and management can focus on issues different than pumping the share price up (and thus creating a ‘natural’ take-over barrier).

German corporate law has, since 2001, clarified its position with regard to the issue of take-over defences, at least as far as the post-bid phase is concerned. The Take-over Act allows management after a tender offer is launched to react by taking into account the interests of the company. The concept of the ‘interest of the firm’ is viewed as allowing the board to take under account other stakeholders’ interests and thus to adopt take-over defences by invoking the potential harmful effects of the acquisition on the employees. This stance was reinforced following the transposition of the Take-over Directive into German Law, in the framework of which Germany opted out of Article 9 that features the board neutrality rule.99xFor an overview of German law's stance vis-à-vis hostile take-overs see Masouros 2013, p. 212. Thus, German corporate law created an environment of relatively lower capital market pressure, which in turn created incentives for long-term strategies during collective bargaining and thus more cooperative industrial relations that eventually interacted with monetary institutions and promoted Germany's trade competitiveness.

German corporate governance institutions were accommodative of the decentralization of German industrial relations and supportive of their cooperative climate. This is because of the institutions of codetermination that endowed German firms with an ‘embedded collectivism’ allowing the shifting to bargaining at the company- and/or plant-level to succeed in restoring exports competitiveness and further because of the insulation from hostile take-overs that reduced capital market pressures on labour and management, allowing them to take the long view in the framework of collective bargaining.

-

4. Conclusion

Capitalism is abundant in contradictions that result in the production of crises. During such crises, capital goes through devaluations that give rise to unemployment, bankruptcies and income inequality. The ability of a nation to resist the forces of devaluation depends on the array of institutional or spatio-temporal fixes it possesses, which can buffer the effects of the crisis, switch the crisis to other nations or defer its effects to the future. Corporate governance configurations in a given social order can function as institutional or spatio-temporal fixes, provided they are positioned within an appropriate institutional environment that can give rise to beneficial complementarities.

Germany seems to resist most effectively the effects of the Great Recession compared with other nations (be it nations of the insider or the outsider model of corporate governance). This article posits that this is due to an institutional complementarity between Germany's corporate governance system, its system of industrial relations and the monetary institutions of the EMU.

Cooperative collective bargaining is viewed upon as a key to the attainment of wage moderation that can boost an export-led growth strategy and increase a nation's competitiveness. The leading of the German system of industry-wide collective bargaining by the metalworking industry that sets the pace for other industries combined with the independence of the Bundesbank allow for a coordinated environment where wage setting is non-inflationary. This endowed Germany with trade competitiveness particularly during the period of the ERM, when the Bundesbank was the ERM's real central bank. Uncoordinated collective bargaining in other Member States resulted in them not benefiting from central bank independence and thus developing inflationary wage setting that eroded their competitiveness during the same period. Because of the asymmetry in the EMU, Germany was able to deepen its trade surpluses and competitiveness vis-à-vis other nations and particularly vis-à-vis those of the periphery. To maintain an inflation-free environment and to finance the trade deficit of its intra-EMU trading partners, Germany recycled its export profits through capital inflows into deficit nations. This led to asset value inflation and the formation of bubbles in the deficit nations who could not turn the inflows into productive activities. The capital outflows resulted in a slow growth rate in Germany that also because of the Stability and Growth Pact had to reverse the capital flows. This led to a ‘sudden stop’ in the periphery nations, bursting of the bubbles and investors’ flight to safety to Germany that hence increased its benefits from the Great Recession by emerging as a safe haven.

German industrial relations, however, would not have been cooperative and accommodative of a wage-moderation climate if it were not for the German institutions of corporate governance. Without its corporate governance institutions, Germany would not have been able to take advantage of the possibilities for a better positioning because of the EMU reality. The success of the company- and/or plant-level employment pacts, which are viewed as key to both wage moderation during the 1990s and 2000s and labour hoarding during the Great Recession, was the result of the ‘embedded collectivism’ that labour-management codetermination institutions have endowed the German corporate edifice with. These institutions have also resulted in a system of ‘negotiated shareholder value’, where the preferences of institutional investors become subject to the preferences of the larger stakeholder coalition that is typical of German corporate governance; this has contributed to an aversion towards downsizings despite the fact that shareholders would stand to benefit therefrom. Finally, the weak capital market pressure that results from the ability of German firms to defend against hostile takeovers allows bargaining parties to adopt the long-term view during collective bargaining and thus reach concessions unattainable in bargaining situations poised with short-termist thinking.

The takeaway is that regardless of the traditional character of a corporate governance system as inside or outside, the resilience with which such system endows a given economy vis-à-vis the effects of an economic crisis and eventually its potency as an institutional or spatio-temporal fix depends on the system's interaction with institutions located in other domains. The addition of the monetary institutions of the EMU to the German institutional equation helps explain the distinctive route that Germany has followed during the Great Recession when compared with its traditional institutional relative, Japan, and widens the range of factors that comparative corporate governance scholarship should henceforth take into account in seeking the ‘one best way’ of regulating the corporation. Bibliography M. Aglietta, Régulation et Crises du Capitalisme: L’ Expérience des Etats-Unis, Calmann-Lévy 1976.

C. Ahmadjian, “Foreign Investors and Corporate Governance in Japan”, in M. Aoki et al. (eds.), Corporate Governance in Japan: Institutional Change and Organizational Diversity, Oxford University Press 2007.

C. Ahmadjian & G. Robbins, “A Clash of Capitalism: Foreign Shareholders and Corporate Restructuring in 1990s Japan”, 70 American Sociological Review 2005, p. 451.

L. Althusser, For Marx (On the Materialistic Dialectic), Verso 1965.

B. Amable, E. Ernst & S. Palombarini, “How Do Financial Markets Affect Industrial Relations: An Institutional Complementarity Approach”, 3 Socio-Economic Review 2005, p. 311.

M. Aoki, “Toward an Economic Model of the Japanese Firm”, 28 Journal of Economic Literature 1990, p. 1.

R. Bispinck, “Betriebsräte, Arbeitsbedingungen und Tarifpolitik”, 58 WSI-Mitteilungen 2005, p. 301.

R. Boyer, “Is a Finance-led Growth Regime a Viable Alternative to Fordism? A Preliminary Analysis”, 29 Economy and Society 2000, p. 111.

S. Clarke, “Crisis of Fordism or Crisis of Capitalism?”, 83 Telos 1990a, p. 71.

S. Clarke, “The Marxist Theory of Overaccumulation and Crisis”, 54 Science & Society 1990b, p. 442.

R. Dore, Stock Market Capitalism: Welfare Capitalism Japan and Germany Versus the Anglo-Saxons, Oxford University Press 2000.

G. Duménil & D. Lévy, The Crisis of Neoliberalism, Harvard University Press 2011.

Eurostat, External and Intra-EU Trade A Statistical Yearbook, Data 1958-2010, Eurostat Statistical Books 2011

J. Franks & C. Mayer, “Corporate Ownership and Control in the UK, Germany and France”, 9 Journal of Applied Corporate Finance 1997, p. 30.

M. Galanis, “The Impact of EMU on Corporate Governance: Bargaining in Austerity”, 33 Oxford Journal of Legal Studies 2013, p. 475.

F. Giavazzi & A. Giovannini, Limiting Exchange Rate Flexibility, MIT Press 1989.

P. Gourevitch & J. Shinn, Political Power & Corporate Control The New Global Politics of Corporate Governance, Princeton University Press 2005.

M. Goyer, “Contextualised Capital: Policy Reforms and Inward Flows in Germany”, 21 German Politics 2012, p. 161.

R. Gumbrell-McCormick & R. Hyman, “Embedded Collectivism? Workplace Representation in France and Germany”, 37 Industrial Relations Journal 2006, p. 473.

T. Haipeter, “Works Councils as Actors in Collective Bargaining: Derogations and the Development of Codetermination in the German Chemical and Metalworking Industries”, 32 Economic and Industrial Democracy 2011, p. 679.

J. Halevi & B. Lucarelli, “Japan's Stagnationist Crises”, 53 Monthly Review 2002, p. 24.

P. Hall & R. Franzese, “Mixed Signals: Central Bank Independence, Coordinated Wage Bargaining, and European Monetary Union”, 52 International Organization 1992, p. 505.

P. Hall & D. Soskice, “An Introduction to Varieties of Capitalism”, in P. Hall & D. Soskice (eds.), Varieties of Capitalism: The Institutional Foundations of Comparative Advantage, Oxford University Press 2001.

D. Harvey, The Condition of Postmodernity. An Enquiry into the Origins of Cultural Change, Wiley 1990.

D. Harvey, The Enigma of Capital and the Crises of Capitalism, Oxford University Press 2011.

D. Harvey, The Limits to Capital, Verso 1982.

D. Harvey, Spaces of Global Capitalism Towards a Theory of Uneven Geographical Development, Verso 2006.

A. Hassel, “The Paradox of Liberalization Understanding Dualism and the Recovery of the German Political Economy”, 52 British Journal of Industrial Relations 2014, p. 57.

B. Herz & W. Röger, “The EMS Is a Greater Deutschmark Area”, 36 European Economic Review 1992, p. 1413.

M. Höpner, “What Connects Industrial Relations and Corporate Governance? Explaining Institutional Complementarity”, 3 Socio-Economic Review 2005, p. 331.

T. Hoshi & A. Kashyap, Corporate Financing and Governance in Japan: The Road to the Future, MIT Press 2004.

T. Hoshi & D. Scharfstein, “The Role of Banks in Reducing the Cost of Financial Distress in Japan”, 27 Journal of Financial Economics 1990, p. 67.

H. Hung, “Rise of China and the Global Overaccumulation Crisis”, 15 Review of International Political Economy 2008, p. 149.

International Monetary Fund, “Changing Patterns of Global Trade”, IMF Policy Paper 2011, Figure 6.1, p. 33. Available at: <www.imf.org/external/np/pp/eng/2011/061511.pdf> (last accessed 28 January 2014).

A. Isogal, “The Transformation of the Japanese Corporate System and the Hierarchical Nexus of Institutions”, in R. Boyer et al. (eds.), Diversity and Transformations of Asian Capitalisms, Routledge 2013.

G. Jackson, M. Höpner & A. Kurdelbusch, “Corporate Governance and Employees in Germany: Changing Linkages, Complementarities and Tensions”, in H. Gospel & A. Pendleton (eds.), Corporate Governance and Labour Management: An International Comparison, Oxford University Press 2005.

B. Jessop, “Finance-Dominated Accumulation and the Limits to Institutional and Spatio-Temporal Fixes in Capitalism”, in S. Jansen et al. (eds.), Fragile Stabilität Stabile Fragilität, Springer VS 2013.

Kommission Mitbestimmung, Mitbestimmung und neue Unternehmenskulturen Bilanz und Perspektiven, Gütersloh, Bertelsmann Foundation 1998.

H. Kraemer & P. Spahn, “Sinn After Boehm-Bawerk: Income Distribution, Capital Flows and Current Account Imbalances in EMU”, in H. Kraemer et al. (eds.), Macroeconomics and the History of Economic Thought, Routledge 2012.

F. Kuroki, “The Relationship of Companies and Banks as Cross-shareholdings Unwind Fiscal 2002 Cross-shareholding Survery”, Nippon Life Insurance Research Working Paper 2003. Available at: <www.nli-research.co.jp/english/economics/2003/eco031118.pdf> (last accessed 28 January 2014).

W. Lazonick, “Organizational Learning and International Competition”, in J. Michie & J. Smith (eds.), Globalization, Growth, and Governance: Creating an Innovative Economy, Oxford University Press 1998.

R. Levine, “Bank-based or Market-based Financial Systems: Which Is Better?”, NBER Working Paper 9138, 2002. Available at SSRN: <http://ssrn.com/abstract=307096> (last accessed 28 January 2014).

J. Mahoney & K. Thelen, “A Theory of Gradual Institutional Change”, in J. Mahoney & K. Thelen (eds.), Explaining Institutional Change: Ambiguity, Agency and Power, Cambridge University Press 2010.

T. Maniatis, “Marxist Theories of Crisis and the Current Economic Crisis”, 41 Forum for Social Economics 2012, p. 6.

D. Marin, “Germany's Super Competitiveness: A Helping Hand From Eastern Europe”, 20 June 2010, VoxEU.org. Available at: <www.voxeu.org/index.php?q=node/5212> (last accessed 28 January 2014).

D. Marin, “The Opening Up of Eastern Europe at 20: Jobs, Skills, and ‘Reverse Maquiladoras’ in Austrian and Germany”, Bruegel Working Paper, July 2010. Available at: <www.bruegel.org/publications/publication-detail/publication/421-the-opening-up-of-eastern-europe-at-20-jobs-skills-and-reverse-maquiladoras-in-austria-and-germany/> (last accessed 28 January 2014).

K. Marx, Capital II, New York, International Publishers 1967a.

K. Marx, Capital III, New York, International Publishers 1967b.

K. Marx, Grundrisse der Kritik der Politischen Ökonomie, Penguin 1973.

P. Masouros, Corporate Law and Economic Stagnation: How Shareholder Value and Short-termism Contribute to the Decline of the Western Economies, Eleven International Publishing 2013.

R. McKinnon, “The Rules of the Game: International Money in Historical Perspective”, 31 Journal of Economic Literature 1993, p. 1.

T. Niechoj et al., “German Labour Costs: A Source of Instability in the Euro Area Analysis of Eurostat Data for 2010”, IMK Report No. 68e, December 2011. Available at: <www.boeckler.de/pdf/p_imk_report_68e_2011.pdf> (last accessed 28 January 2014).

T. Noda, “Determinants of the Timing of Downsizing Among Large Japanese Firms: Long-term Employment Practices and Corporate Governance”, 64 Japanese Economic Review 2013, p. 363.

R. Posner, A Failure of Capitalism, Harvard University Press 2009.

J. Priewe, “Economic Divergence in the Euro Area. Why We Should Be Concerned”, in E. Hein et al. (eds.), European Integration in Crisis, Metropolis 2007.

D. Raess, “Export Dependence and Institutional Change in Wage Bargaining in Germany”, International Studies Quarterly 2013, p. 1.

M. Roe, Political Determinants of Corporate Governance Political Context, Corporate Impact, Oxford University Press 2003.

K. Rogoff, “The Optimal Degree of Commitment to an Intermediate Monetary Target”, 11 Quarterly Journal of Economics 1985, p. 1169.

M. Russo & G. Tullio, “Monetary Conditions Within the European Monetary System: Is There a Rule?”, in Policy, Coordination in the European Monetary System, Occasional Paper 61, IMF 1998.

H.W. Sinn & T. Wollmershäuser, “Target Balances and the German Financial Account in Light of the European Balance of Payments Crisis”, CESiFO Working Paper No. 4051, 2012. Available at: <www.cesifo-group.de/DocDL/cesifo1_wp4051.pdf>? (last accessed 28 January 2014).

D. Soskice & T. Iversen, “Multiple Wage-Bargaining Systems in the Single European Currency Area”, 14 Oxford Review of Economic Policy 1998, p. 110.

E. Stockhammer, “Financialization, Income Distribution and the Crisis”, 279 Investigacion Economica 2012, p. 39.

E. Stockhammer, “Wage Moderation Does Not Work: Unemployment in Europe”, 39 Review of Radical Political Economics 2007, p. 391.

W. Streeck, “Pay Restraint Without Incomes Policy: Institutionalized Monetarism and Industrial Unionism in Germany”, in R. Dore et al. (eds.), The Return of Incomes Policy, London, Pinter 1994.

W. Streeck, “The Transformation of Corporate Organization in Europe: An Overview”, MPIfG Working Paper 01/8, December 2001.

T. van Treeck et al., “Finanzsystem und wirtschaftliche Entwicklung in den USA und in Deutschland im Vergleich”, 2007. Available at: <www.boeckler.de/pdf/wsimit_2007_12_treeck.pdf> (last accessed 28 January 2014).

Y. Varoufakis, “From Contagion to Incoherence Towards a Model of the Unfolding Eurozone Crisis”, 32 Contributions to Political Economy 2013, p. 51.

S. Vitols, “Negotiated Shareholder Value: The German Variant of an Anglo-American Practice”, 8 Competition & Change 2004, pp. 357-374.

T. Yamada & Y. Hirano, “How Has the Japanese Mode of Régulation Changed? The Whereabouts of Companyism”, in R. Boyer et al. (eds.), Diversity and Transformations of Asian Capitalisms, Routledge 2013.

S. Zagelmeyer, “Brothers in Arms in the European Car Wars: Employment Pacts in the EU Automobile Industry”, 8(2) Industrielle Beziehungen 2001, p. 149.

-

1 Marx 1967a, p. 316.

-

2 Jessop 2013, p. 310.

-

3 See Clarke 1990a, p. 71.

-

4 See Aglietta 1976.

-

5 For an account of the events leading to the transformation of the global economy starting from the 1970s, see Masouros 2013, pp. 55 et seq.

-

6 For Europe, see Stockhammer 2007, pp. 391, 394-395, illustrating the declining wage share (= real unit labour costs in the business sector); for the US see Duménil & Lévy 2011, p. 49.

-

7 Marx 1967b, p. 244.

-

8 For the rising trend of household debt in the United States, see Harvey 2011, p. 18; for the rising trend of household debt in Europe (although for a shorter time-period) see Stockhammer 2012, pp. 39, 55.

-

9 Jessop 2013, p. 318.

-

10 See Boyer 2000, pp. 111-112.

-