-

1 Introduction

Cooperatives represent a very important organizational arrangement in world food and agriculture.1xAccording to the World Co-operative Monitor of the International Co-operative Alliance (ICA), in 2012 the total turnover of 523 agricultural cooperatives in 30 countries was approximately $598.90 billion. The 2014 report where this information was derived from can be found at <https://dl.dropboxusercontent.com/u/24617037/QRcode/WCM2014.pdf>. A recent, in-depth study of these organizations in all European Union (EU) Member States and selected non-EU OECD countries reveals that there exists not a single country in the world with an advanced food and agriculture system, in which agricultural cooperatives do not play a key role.2xBijman et al. 2012. However, a common misconception is that all agricultural cooperatives are the same.3xIn plain English, this is often expressed, as ‘the co-op is a co-op is a co-op’. Yet, even a scant inspection of the extant literature reveals that this is not the case.4xSee, for example, Iliopoulos & Cook 2013; Cook & Burress 2009 and Cook 1995. Advances in the theory of the cooperative firm during the last 30 years have shown that cooperatives may differ significantly with respect to their organizational architecture.5xSee, for example, Chaddad & Cook 2004; Hendrikse & Veerman 2001 and Cook & Iliopoulos 1999. The term organizational architecture refers primarily to two key questions any institutional arrangement has to answer in an efficiency-maximizing way. First, which groups of patrons should be the owners of the organization and, second, how does the organization distribute ownership rights to its owners?6xHansmann 1996.

Based on the single criterion of whether or not non-patrons are entitled to become owners of the cooperative, we observe more than a few very different types of agricultural cooperatives.7xChaddad & Cook 2004. Considering also corporate governance choices in our inquiry, we find that agricultural cooperatives adopt one out of the four basic corporate governance models or any of the corresponding variations.8xChaddad & Iliopoulos 2013. But why do agricultural cooperatives choose to adopt ownership and governance features that distant them from the traditional cooperative model? This is because they need to provide complementary incentives to the cooperative’s stakeholders in order to (1) attract risk capital and (2) optimize collective decision-making costs.9xCook & Iliopoulos 2000. In replying to external and intra-cooperative pressures, agricultural cooperative leaders design and implement incentive mechanisms and strategies to combat intra-organizational challenges. Hence arises the need to implement an efficient and sustainable organizational architecture. Yet, in making these crucial choices, agricultural cooperatives are faced with several important trade-offs that have significant implications both for farmers and their cooperatives but also for society as a whole.10xFor example, in achieving food security or renewable energy consumption goals. This article identifies these trade-offs and discusses how agricultural cooperatives deal with them. In doing so, the article informs both scholarly research and practitioners’ work.

The remaining of the article is structured in four sections. Section 2 gives a brief presentation of the basic concepts in the ownership and governance of economic organizations. The ensuing section summarizes the relevant literature and proffers an overview of ownership and governance choices available to agricultural cooperatives. It also identifies and discusses important trade-offs agricultural cooperatives face in making their key ownership and governance choices. The final section proffers nine observations derived from the preceding discussion and concludes the article with suggestions for future research. -

2 Ownership and Governance: Basic Economic Concepts

Ownership is a very elusive concept even with respect to simple physical assets.11xMilgrom & Roberts 1992. It becomes, though, even more complicated in the case of large business organizations, which bundle together many assets and "who has what" decision rights may be unclear. Economic analyses of ownership have focused mainly on two issues: the possession of residual decision rights and the allocation of residual returns. Residual decision rights are defined as the rights to make any decision regarding the use of an asset that is not explicitly attenuated by law or assigned to another party by contract. The importance of the residual decision rights derives from the difficulty of writing contracts that specify all the control rights on complicated assets exchanged in complex, recurrent transactions. Due to their importance, ownership is usually defined as the possession of residual decision or control rights.12xGrossman & Hart 1986. Residual control rights are assigned to the parties making relationship-specific investments whose quasirents13xA quasirent is “the difference between the value created by a resource in a particular relation with respect to the value created in its best alternative relation or use (rent), minus the cost of search for and transfer to these alternative relations” (Grandori 2001, p. 237). are under risk due to the possibility for hold-up behaviour.14xThe hold-up problem arises when two factors are present: (1) parties to a future transaction must make non-contractible relationship-specific investments before the transaction takes place and (2) the specific form of the optimal transaction (e.g. quality-level specifications, time of delivery, what quantity of units) cannot be determined with certainty beforehand. The hold-up problem is a situation where two parties may be able to work most efficiently by cooperating but refrain from doing so due to concerns that they may give the other party increased bargaining power and thereby reduce their own profits. When party A has made a prior commitment to a relationship with party B, the latter can ‘hold up’ the former for the value of that commitment. The hold-up problem leads to severe economic costs and might also lead to underinvestment (Rogerson 1992).,15xHart 1995.

Further, economic theory suggests two types of control rights: decision control rights, which refer to the ratification and monitoring of decisions, and decision management rights, which relate to the initiation and implementation of decisions.16xFama & Jensen 1983. The allocation of these subdecision rights has a bearing on the allocation of formal and real (i.e. effective) authority within organizations. Yet, having formal authority does not automatically grant someone real authority.17xAghion & Tirole 1997, p. 2.

Another conceptual way to think of the owner is the residual claimant, the person who is eligible to receive any net income that the firm produces. That is, the owner is entitled to whatever remains after all the revenues have been collected and all debts, expenses and other contractual obligations have been paid. Net income is conceived of as the residual returns – the amount that is left after everyone else has been paid.18xMilgrom & Roberts 1992. Similarly to residual control, the notion of residual returns is intimately tied to contractual incompleteness. Under complete contracting, the division of wealth in each eventuality would be specified contractually, and there would be no economic returns that could usefully be thought of as residual. Just as the allocation of residual control can be fuzzy in the case of complex assets such as firms, the notion of residual returns is vague as well. For example, under certain circumstances, lenders are the residual claimants. According to the property rights and agency theories, the owners of a firm are its residual claimants.19xAlchian & Demsetz 1972; Fama 1980 and Fama & Jensen 1983. The same theories suggest that when it is possible for a single individual to both have the residual control and receive the residual returns, the residual decisions made will tend to be efficient. In contrast, if only part of the costs or benefits accrue to the party making the decision, then that individual will find it in his or her personal interest to ignore some of these effects, frequently leading to inefficient decisions. Properly combining the two aspects of ownership – residual control and residual returns – provide strong incentives for the owner to maintain and increase an asset’s value.20xAlchian & Demsetz 1972. Yet, in the case of complex organizations, there is necessarily separation of ownership and control that potentially leads to agency issues.21xBerle and Means 1932.

The assignment of residual control and residual income rights provides a very useful basis for distinguishing between different ownership and governance structures. For example, an investor-oriented firm (IOF)22xFor example, an open corporation, notably the stock listed corporation. can be defined as a firm with unrestricted residual claims that are non-redeemable but freely tradable in secondary equity capital markets. The horizon of its residual claims is also unlimited because they are rights in the net cash flows for the life of the organization. In addition, residual claimants are not required to assume any other role or function in the firm. The unrestricted nature of common-stock residual claims enables the efficient allocation of risk and the specialization of risk-bearing and decision-making functions in this type of corporations.

In contrast to open corporations, non-corporate organizational forms usually add restrictions on residual claims in the sense that they may affect asset investment and use. For example, traditional agricultural cooperatives can be defined based on the following property rights characteristics: (1) ownership rights are restricted to member-patrons; (2) residual income rights are non-transferable, non-appreciable and redeemable; (3) residual income is distributed to members in proportion to patronage; and (4) residual decision rights are distributed to member-patrons on the basis of either the one-member-one-vote rule or in proportion to patronage.23xUsually with a preset upper limit of votes per member. This definition captures the essence of cooperatives in terms of ownership rights while in line with the observed variety of cooperative models across countries and even within countries.24xChaddad & Iliopoulos 2013. -

3 Ownership and Governance Choices of Agricultural Cooperatives

We are interested in identifying the ownership and governance options of agricultural cooperatives as well as unravelling the trade-offs they face in making these choices. We start with the first line of inquiry, while the latter follows.

Based on how ownership rights are defined and assigned to cooperative stakeholders tied to the cooperative contractually (members, patrons, employees and investors), a number of basic, discrete cooperative models are identified.25xChaddad & Cook 2004. In the case that ownership rights are restricted to member-patrons, equity capital is provided by members alone. Defined in the preceding section, traditional agricultural cooperatives also come in various forms such as those with vertical investments26xThe term ‘traditional cooperatives with vertical investments’ refers to traditional agricultural cooperatives that have invested in limited liability companies or other forms of strategic alliances as a means of entering other vertical stages of their food supply chains (e.g. production of value-added food items or agricultural inputs). or others transitioning to new-generation cooperatives.27xCook & Chaddad 2004. Given that the aforementioned restriction holds, three additional types of cooperatives are identified: proportional investment, member investor and new generation. In proportional investment cooperatives, ownership rights are restricted to members – non-transferable, non-appreciable and redeemable – but members are expected to invest in proportion to patronage. A variation of this model is the proportional investment cooperative with vertical investment.28xIbid. As membership heterogeneity increases, proportional investment cooperatives tend to operate more like traditional cooperatives and, after realizing that, they adopt capital management policies to ensure proportionality of internally generated capital such as separate capital pools and base capital plans.29xIbid.

Member-investor cooperatives distribute returns to members in proportion to shareholdings in addition to patronage. Usually, this is achieved by distributing dividends in proportion to shares and allowing appreciation of cooperative share value. A variation of the basic member-investor cooperative is the member-investor cooperative with vertical investment.30xIbid.

New-generation cooperatives are characterized by ownership rights in the form of tradable, appreciable and non-redeemable delivery rights restricted to current member-patrons. Additionally, member-patrons are required to purchase delivery rights in proportion to their expected patronage so that usage and capital investment are proportionally aligned. The basic new-generation model is the basis for the development of new-generation cooperatives with vertical investments and cooperatives adopting the collaborative new-generation model.31xIbid.

The four types of cooperatives, in which ownership rights are restricted to member-patrons, have developed vertical investment strategies, such as investments in limited liability companies, joint ventures or other forms of strategic alliances.32xIbid. Some traditional cooperatives also have made or are attempting to make a transition to a new-generation cooperative ownership structure.

When ownership rights are not restricted to member-patrons, three additional types of organizational architecture emerge: cooperatives with capital-seeking entities, investor-share cooperatives and IOFs.33xChaddad & Cook 2004. In the first of these organizational forms, investors acquire ownership rights in a separate legal entity wholly or partly owned by the cooperative. While similar to the vertical investment strategies of the previously discussed set of cooperative models, the two differ by the degree of control conceded and the importance of permanent capital contributions.

In the case of investor-share cooperatives, we observe the issuance of more than one class of shares to different owner groups, such as non-voting fixed returns preferred stock and non-voting publicly tradable, common stock. However, it is member-patrons who maintain their traditional ownership rights linked to patronage of the cooperative and who are still entitled to control rights.

The last discrete ownership choice of agricultural cooperatives is to convert into an IOF, which represents an exit strategy.34xCook & Burress 2009. Even if farmer-members intend to maintain a controlling share of ownership rights, usually outside investors manage to acquire more than 51% of the shares in the IOF. This is due to the fact that in the resulting IOF, both the structure and the objective of the firm are necessarily altered. Very few conversions of agricultural cooperatives to IOFs have been reported (e.g. Schrader 1989). In some European countries,35xFor example, in Finland and the Netherlands; see Iliopoulos 2014. agricultural cooperatives use the PLC structure, and this might have acted as a shield from the threat of a hostile take-over by an IOF.36xIliopoulos 2014. The PLC is an investor-oriented, public limited company owned by a cooperative association. The latter is exclusively a governance unit while most of the cooperative’s value-added business takes place through the former. In the past, PLCs were exclusively owned by cooperative associations and their individual members. In recent years, however, an increasing number of these PLCs have issued stock to non-member investors. In this way and through the PLC’s wholly or partially owned subsidiaries, the cooperative raises risk capital in addition to that contributed by members. In countries where the governance and business units are under the same organization (the cooperative), the need to finance growth has in some cases led to IOFs taking over the cooperative. In the USA, some cooperatives have converted into a farmer-owned limited liability company to optimize collective decision-making costs, improve their access to non-member capital and become eligible for tax breaks.37xChaddad & Cook 2007; Fulton & Hueth 2009; Lamprinakis & Fulton 2011; Lind 2011.

The diversity of ownership structures adopted by agricultural cooperatives around the globe is not matched by a similar variety of corporate governance models implemented by these organizations.38xBijman, Hendrikse & Van Oijen 2013. According to a recently proposed typology, agricultural cooperatives adopt one out of the following corporate governance models: traditional, extended traditional, managerial and corporate.39xChaddad & Iliopoulos 2013.

The traditional model includes two mandatory bodies: the general assembly (GA) and the board of directors (BoD). In some countries, a supervisory committee (SC) is mandatory by law. Solely the BoD, whose members are elected by the GA, performs decision management. Usually based on the number of votes received by the GA, the members of the board allocate among themselves duties and responsibilities (e.g. the member who received the most votes is elected as the chairman). The GA of members exercises ex post decision control based on an equal or proportional allocation of residual control rights, while the BoD exercises ex ante decision control and decision management except on certain types of decisions requiring GA approval.

The extended traditional governance model differs from the traditional one in that all operational decisions are delegated to professional management hired by the BoD. That is, in this model, the BoD maintains the ex ante decision control function, but decision management is carried out by a professional manager. In some countries (e.g. the Netherlands), the law requires that above a certain number of employees, the GA appoints the members of a board of commissioners (BoC).40xBijman, Hendrikse & Van Oijen 2013. The BoC’s ex post decision control function focuses on ensuring that the interests of all stakeholders are taken into consideration.

In the managerial model, the BoD and professional management are consolidated, thus eliminating one level of governance. The BoD is responsible for decision management functions performed exclusively by professionals who are not member-patrons. Consequently, the managerial model entrusts both formal and real authority to professional management. While formal control is still vested in the GA, it is professional managers that make all operational and strategic decisions. The SC (or the BoC in larger cooperatives) exercises ex post control over decisions made by the BoD.

In the corporate model, the BoD and the SC or BoC are consolidated. Both members and non-members (usually experts) participate in this extended BoD, but bylaws may stipulate that two-thirds of BoD members are also member-patrons of the cooperative. In this corporate governance model, professional managers exercise both formal and real authority. Most decisions are delegated to managers, and the BoD is merely responsible for ex post decision control.

The traditional model is primarily adopted in parts of Southern Europe and South America, while the extended model is the predominantly adopted model in most parts of the world, including Northern Europe, North America and Oceania. The managerial and corporate models have emerged in recent years in Northern Europe and, particularly, in the Netherlands.41xBijman, Hendrikse & Van Oijen 2013. Next, we turn to how agricultural cooperatives decide on which ownership and corporate governance model to adopt and the trade-offs they face in making these choices. -

4 Choosing among Ownership and Governance Alternatives by Agricultural Cooperatives

The aforementioned ownership choices have resulted, at least partially, from the constant, conscious efforts of cooperative leaders to ameliorate a set of constraints faced by traditional agricultural cooperatives and combat the negative consequences of member interest heterogeneity. Both of these sources of inefficiency have their roots in the period when farmer-members and their leaders designed the organizational architecture of their cooperative.42xIliopoulos & Cook 2013. The constraints that have been identified and studied in the scholarly literature include the free rider, horizon, portfolio, control and influence cost problems.43xSee, for example, Cook 1995; Cook & Iliopoulos 2000. The first three refer to the disincentives facing members of traditional cooperatives to contribute significant amounts of risk capital to their cooperative due to the vaguely defined property rights of these organizations.44xCook 1995. The last two refer to the costs of monitoring non-member management and the costs of collective decision-making.45xSee, for example, Hansmann 1996; Iliopoulos & Hendrikse 2009.

The free rider problem emerges in cooperatives when ownership rights are non-tradable, insecure, unassigned or vaguely defined. The external free rider constraint is a common-resource problem. Cooperative ownership rights are not well suited and enforced to ensure that current member-patrons, or current non-member-patrons, bear the full costs of their actions and/or receive the full benefits they create. This situation occurs particularly in open-membership cooperatives. The example usually cited refers to the case of a processing tomato producer who refuses to join the membership of a tomato bargaining association but captures the benefits of the negotiated terms of trade. A more complex type of free rider problem, the insider free rider problem, occurs when dealing with common-property issues. This occurs when new members obtain the same patronage and residual rights as existing members and are entitled to the same payment per unit of patronage. This set of equally distributed rights combined with the lack of a market to establish a price for residual claims that reflects accrued and present equivalents of future earning potential creates an intergenerational conflict. Because of the dilution of the rate of return to existing members, a disincentive is created for them to invest in their cooperative.46xCook 1995.

The horizon problem refers to the disincentive for cooperative members to invest in long-term projects. Benefits flowing to the patron instead of to the investor are also the genesis of this problem. Specifically, the horizon problem occurs when a member’s residual claim on the net income generated by an asset is shorter than the productive life of that asset.47xCook & Iliopoulos 2000. This problem is caused by restrictions on transferability of residual claimant rights and the lack of liquidity through a secondary market for the transfer of such rights. The horizon problem creates an investment environment in which there is a disincentive for members to contribute to growth opportunities. The severity of this problem intensifies when considering investment in research and development, advertisement and other intangible assets. Consequently, there is pressure on the board of directors and management to (1) increase the proportion of the cooperative’s cash flow devoted to current payments to members relative to investment and (2) accelerate equity redemptions at the expense of retained earnings. This causes fierce problems of raising risk capital from members.

The portfolio problem can be viewed from the cooperative firm’s point of view as another equity acquisition constraint. The lack of transferability, liquidity and appreciation mechanisms for the exchange of residual claims prevents members from adjusting their cooperative asset portfolios to match their personal-risk preferences. The cause of this problem is again the tied-equity issue – the investment decision is ‘tied’ to the patronage decision. Therefore, members hold suboptimal portfolios, and those who are forced to accept more risk than they prefer will pressure cooperative decision-makers to rearrange the cooperative’s investment portfolio, even if the reduced-risk portfolio means lower expected returns.48xIliopoulos and Cook 2013.

The control problem refers to the multiple types of agency costs associated with the divergence of interests between the principals (members) and the agent (professional management). The lack of a secondary market for cooperative residual claims makes monitoring of agents a difficult task. This task is further complicated by the fact that subgroups of member-patrons tend over time to have very heterogeneous preferences and thus the cooperative’s objective function may become ambiguous.49xCook & Burress 2009. On the other hand, member-patrons, at least in some types of agricultural cooperatives, may be well positioned to monitor management effectively.50xHansmann 1996.

The influence cost problem refers to the class of costs that inevitably arise in any organization when decisions affect the distribution of wealth or other benefits among members or constituent groups of the organization, and, in pursuit of their selfish interests, the affected individuals or groups attempt to influence the decision to their benefit.51xIliopoulos & Hendrikse 2009. In legal terms, this might lead to cases of minority oppression. The influence cost problem may become a major source of inefficiencies in agribusiness cooperatives. Several crucial decisions entail the distribution of wealth among member-patrons and thus may provoke and influence attempts by members. The allocation of overhead costs, the assessment of members’ product quality and the geographical location of a new investment are but a few examples of such decisions.52xHansmann 1996.

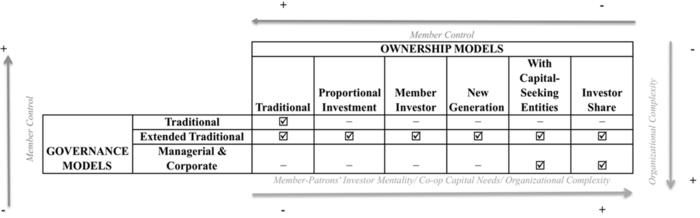

In order to create incentives for members to contribute risk capital and combat the negative consequences of diachronically increased member interest heterogeneity, agricultural cooperatives may spend a considerable amount of time on experimenting with minor changes in bylaws and organizational policies.53xCook & Burress 2009. In terms of ownership rights definition and distribution, the cooperatives’ goal during this phase is twofold: (1) to provide their members with powerful incentives to contribute risk capital and (2) to ameliorate the negative externalities of frictions due to increased preference/interest heterogeneity. This is achieved by giving members additional and more clearly defined ownership rights in their cooperative and is manifested as a move away from the traditional cooperative model to the proportional investment, the member investor and the new-generation ownership models. However, under certain circumstances related to the industry of the cooperative and market conditions, but also to intra-cooperative characteristics,54xFor example, degree of the members’ interest heterogeneity. this tinkering may not suffice to address the above-mentioned issues. At this point, cooperatives are faced with a crucial decision.55xIliopoulos 2014. Depending on the persistence of the problems and environmental pressures, the cooperative may decide to distribute residual claimant rights to non-member investors. These may come with or without corresponding residual control rights being distributed to outside investors. Thus for a member, the cost of not investing adequate amounts of risk capital in his or her cooperative can be conceived as a loss of control over the organization. In order to avoid having outside-investor control – at least partially – some cooperatives create separate capital-seeking entities and share the ownership of these entities with outside investors. Thus, it seems to be the need to ameliorate the vaguely defined property rights constraints and align members’ interests that have given rise to the adoption of non-traditional agricultural cooperative features. Figure 1 presents the ownership and governance models and identifies the feasible combinations adopted by agricultural cooperatives in various countries. It also shows the major trade-offs members and their cooperatives face when moving from one choice to another.Trade-offs in choosing ownership and governance features in agricultural cooperatives

Moving from the traditional cooperative to the left to the investor-share cooperative to the far right, we observe three major trade-offs. First, as members increasingly incorporate investor preferences56xThat is, as opposed to patron preferences. into their individual objective functions, they are willing to lose varying degrees of control over their cooperatively owned business. This move towards the investor-share model also implies an increasing need of the cooperative entity for risk capital to invest in projects that will safeguard the cooperative from external competitive pressures and/or enable it to seek offensively higher margins in other levels of vertical food supply chains.57xIliopoulos & Cook 2013. Moving along this continuum, we also observe that as organizational complexity increases, the cooperative distributes more and more clearly defined residual claimant rights to member-patrons. For example, the cooperative may modify its bylaws so as to allow proportional voting,58xCook & Iliopoulos 2000. departing from the ICA principle of ‘one man, one vote’. Simultaneously the cooperative may also distribute residual income rights in more equitable ways. The adoption of separate product, capital and decision-making pools in multiproduct and multipurpose cooperatives are relevant examples of this trade-off. In agricultural cooperatives in which the majority of members do not take action to implement a separate pool for a minority of members (e.g. regular versus organic milk), if the suppressed members cannot exercise convincingly their voice option, they usually will leave the cooperative and may start a new collective entrepreneurship venture.59xStaatz 1987. The adoption of all these new rules and policies may also serve as a shield against cooperative degeneration.60xThe term ‘cooperative degeneration’ comes from the game theoretical literature and refers to any type of organizational decline; see Cook & Burress 2009. Hence the aforementioned trade-off may be viewed as a means of protecting member-patrons from outside invasions.

In the context of this article, organizational complexity refers to the condition of having many diverse and autonomous but interrelated and interdependent components or parts linked through dense interconnections. In the framework of an organization, complexity is associated with interrelationships of the individuals, their effects on the organization and the organization’s interrelationships with its external environment.61xKeskinen, Aaltonen & Mitleton-Kelly 2003. Given this definition, we can safely assume that, ceteris paribus, organizational complexity is higher in agricultural cooperatives than investor-oriented firms, not least because of the possibility of member interest heterogeneity-induced conflicts. However, we do not assume that all types of organizational complexity result in lower organizational efficiency. We assume that organizational complexity neither causes, nor is caused by heterogeneity of members’ interests/preferences alone. Let us turn now to the choice of the governance model.

In order to improve the efficiency of decision-making, agricultural cooperatives in some countries have abandoned the traditional governance approach and even the extended traditional one in favour of the managerial or corporate model. It seems clear that this choice has been dictated by the increasing organizational complexity and the consequent need to speed up decision-making by professionals instead of farmer-members. Two major trade-offs might be observed as agricultural cooperatives choose among governance alternatives. The first is between organizational complexity and formal/real control of the cooperative by member-patrons. As organizational complexity increases and thus the need for improved decision-making efficiency, the cooperative moves from the traditional to the extended traditional and then to the managerial and corporate governance models. At the same time, though, their members lose more and more formal and probably also real control of the cooperative. Of course, the decision-making context in which agricultural cooperatives operate is usually more complex in real-life situations. In some cases, such a process may take many years before completion, not least because of cultural preferences or opportunistic behaviour of cooperative leaders.62xSee Iliopoulos & Valentinov 2012.

The other major trade-off is between monitoring costs and the costs of collective decision-making. As cooperatives adopt more and more of the non-traditional governance features, the costs of collective decision-making are supposedly becoming lower and lower. Yet, this achievement may come at the expense of higher management monitoring costs. If agency costs are relatively low in agricultural cooperatives, then this hypothesized lost member control may not pose a serious threat to agricultural cooperatives. Hansmann adopts this approach to intra-cooperative agency costs.63xHansmann 1996. He argues that farmer-members are in a relatively good position to monitor management effectively because income received from the cooperative represents their major income source. Other scholars, though, argue that farmer-members are in a weak position to monitor management effectively. These authors argue that this is because farmer-members lack the necessary knowledge, are not facilitated by a secondary market mechanism and face a severe free rider problem with respect to monitoring the management.64xSee, for example, Iliopoulos & Cook 2013; Chaddad & Cook 2004 and Vitaliano 1983. If these authors are correct, then the cooperative may end up not serving the long-run needs of its members. This may be observed more often as organizational complexity rises and cooperative degeneration is accelerated.

The aforementioned trade-offs seem to imply that there must exist a point of (temporary) equilibrium where the allocation of residual claim and control rights, the prevailing mentality of members (patron vs. investor) and membership heterogeneity meet and result in an optimum result.65x‘Optimum result’ in this context should be read as optimum from the members’ point of view. Locating this point, though, is not possible through standard economic optimization techniques. On the contrary, it requires a trial-and-error effort and, in many cases, the adoption of the second-best choice is the only feasible alternative.

By inspecting Figure 1, we can infer that the following nine combinations of governance-ownership models are both theoretically feasible and have been observed in various countries:Traditional-Traditional

Extended Traditional-Traditional

Extended Traditional-Proportional Investment

Extended Traditional-Member Investor

Extended Traditional-New Generation

Extended Traditional-With Capital-Seeking Entities

Extended Traditional-Investor Share

Managerial/Corporate-With Capital-Seeking Entities

Managerial/Corporate-Investor Share

Trade-offs become increasingly important as we move from the traditional-traditional model to non-traditional combinations of governance and ownership. Not surprisingly, organizational complexity and non-member-patron control both increase as we move towards the managerial/corporate-investor-share model.

Are all of these nine combinations sustainable in the long run? This question cannot be answered with any certainty. Given that most of these combinations of governance and ownership features are relatively new, we lack crucial information that would allow us to evaluate them. Many years may pass before we can infer the prospects of each new governance-ownership model. Until very recently, ownership and corporate governance issues in cooperatives were studied separately.66xSee Chaddad & Iliopoulos 2013. Yet the above discussion reveals that the choice of ownership and governance models implies trade-offs crucial for the cooperative’s organizational efficiency. -

5 Observations and Concluding Remarks

The above discussion of ownership and governance choices in agricultural cooperatives allows us to make the following observations:

Observation 1: A co-op is not a co-op is not a co-op

Given the observed variation in ownership and corporate governance features adopted by agricultural cooperatives, it seems no longer meaningful to speak of ‘the cooperative’. Instead, shedding light on these features and their combinations adopted by each individual cooperative may be a prerequisite to understanding these economic organizations. If adopted by policymakers at various levels, such an approach would have multiple positive consequences.67xSee Iliopoulos 2013.

Observation 2: Collective decision-making and cooperative capital

The need for risk capital that members cannot or are not willing to invest in their cooperative seems to explain the agricultural cooperatives’ decision to allow non-patron investors. Whether this represents a stronger incentive than the cooperatives’ need to improve the efficiency of collective decision-making by appointing non-member directors on the board is an ambiguous and largely empirical issue.

Observation 3: Investor mentality and non-member investment

As farmer-members start thinking more and more as investors rather than as patrons, they are increasingly willing to accept non-member investors. Whether they are also willing to accept partial control of the cooperative by these outside investors is questionable. However, a probably accurate indicator of their willingness is whether the cooperative distributes residual control rights to the cooperative itself or to a separate legal entity.

Observation 4: Provision of intra-cooperative incentives is bounded

There seems to exist an upper limit to the risk capital farmer-members can provide their cooperative with. Beyond that point, providing member-patrons with additional incentives in order to attract more capital does not work. However, this should not be taken to imply that agricultural cooperatives do not need to design their organizational architecture as if incentives did not matter. Research in various economic, cultural and policy contexts has shown that cooperatives can avoid degeneration only by designing and implementing a set of multiple, advanced and complementary incentive instruments that target, albeit in a different way, all subgroups of stakeholders tied contractually to the cooperative.68xSee, for example, Lichbach 1996.

Observation 5: Efficient organizational architecture and trade-offs

Attracting member and/or non-member risk capital, increasing organizational complexity and allowing non-member or professional management control of the cooperative are not decisions that cooperatives do independently of each other. On the contrary, the need to design an efficient and sustainable organizational architecture forces cooperative members and their leaders to consider a number of important trade-offs and sometimes make very hard decisions. The aforementioned parameters represent dimensions of these trade-offs.

Observation 6: Balancing trade-offs is a constant battle

During its lifecycle, each agricultural cooperative makes several crucial decisions, which are informed by corresponding trade-offs. Finding the right balance between these trade-offs is a non-trivial task. While initially these trade-offs might be viewed as constraints, a closer look may reveal that they are also important in protecting member-patrons. For example, when some members start acting more and more like investors instead of patrons, the realization that they may have to forgo some of their control rights over the cooperative may act as a wake-up call.

Observation 7: Organizational complexity and property rights

In many cases, as cooperative organizational complexity increases, so does the heterogeneity of members’ interests (is the course of events the other way around: due to increased heterogeneity, the complexity of the organization increases?). In order to minimize the negative consequences of higher organizational complexity, many cooperatives design combinations of complementary incentive mechanisms. This process usually starts by clarifying property rights and distributing them in more equitable ways.69xFor example, by allowing proportional (according to volume of patronage) voting in the general assembly and adopting separate voting pools per product or geographic region.

Observation 8: Membership heterogeneity70xIn this paper, the term ‘membership heterogeneity’ refers primarily to heterogeneity of members’ interests and/or preferences. and organizational complexity

Although not necessarily only negative, heterogeneity in preferences and interests among a cooperative’s membership can definitely have devastating effects on the organization’s long-term prospects.71xCook & Burress 2009. Given, however, that heterogeneity tends to increase over the lifecycle of a cooperative, choices made with respect to the organizational architecture become very important. Membership heterogeneity inflates organizational complexity in ways that have yet to become the focus of scholarly work.

Observation 9: Tinkering has its limits

Despite the efforts of agricultural cooperatives to avoid intra-organizational conflict by making minor changes in bylaws and cooperative policies that result in temporary relief, the time comes when the cooperative needs to consider making more dramatic changes to ensure future survival. Exiting through liquidation, merger or otherwise represents one of these options.72xIliopoulos 2013. Other choices include reinventing the cooperative or, simply, keeping up with the status quo.73xIliopoulos & Cook 2013. Of course, each and all of these choices have their pros and cons.

Observation 10: Assessment of organizational architecture

Assessing the efficiency and sustainability of the ownership and corporate governance model adopted by an agricultural cooperative is feasible only in the long run. Given the resilience of the traditional cooperative model over such a long period of time, drawing conclusions on the advantages and disadvantages of each new cooperative model is extremely difficult. Yet, it seems that we know enough about the consequences of certain ownership and governance choices that cooperatives make early on their life cycle.

These observations inform a number of hopefully useful conclusions. First, today we know much more about the internal organization of agricultural cooperatives than what we knew just 20 years ago. Yet, there is so much more to learn if we avoid research inertia. Second, filling the existing knowledge gaps necessitates the adoption of multidisciplinary and transdisciplinary approaches. Law and economic issues are just an example of the need to use multiple lenses in studying intra-cooperative organizational issues.

Third, multiple country comparisons may provide insights that are not available through studies that focus on a country or region. However, we lack theoretical frameworks that would enable such a comparative research approach. Research towards these directions would highly benefit scholars, practitioners and policymakers alike. Bibliography P. Aghion & J. Tirole, “Formal Authority in Organizations”, 105 Journal of Political Economy, 1997, pp. 1-29.

A.A. Alchian & H. Demsetz, “Production, Information Costs, and Economic Organization”, 62 American Economic Review, 1972, pp. 777-795.

A. Berle & G. Means, The Modern Corporation and Private Property, New York, Macmillan 1932.

J. Bijman, G. Hendrikse & A. van Oijen, “Accommodating Two Worlds in One Organization: Changing Board Models in Agricultural Cooperatives”, 34 Managerial and Decision Economics 3-5, 2013, pp. 204-217.

J. Bijman, C. Iliopoulos, K.J. Poppe, C. Gijselinckx, K. Hagedorn, M. Hanisch, G.W.J. Hendrikse, R. Kühl, P. Ollila, P. Pyykkönen & G. van der Sangen, Support for Farmers’ Cooperatives: Final Report, Wageningen, the Netherlands, Wageningen UR 2012.

F.R. Chaddad & M.L. Cook, “Understanding New Cooperative Models: An Ownership-Control Rights Typology”, 26 Review of Agricultural Economics 3, 2004, pp. 348-360.

F.R. Chaddad & M.L. Cook, “Conversions and Other Forms of Exit in U.S. Agricultural Cooperatives”, in K. Karantininis & J. Nilsson (eds.), Vertical Markets and Cooperative Hierarchies: The Role of Cooperatives in the Agri-Food Industry, Dordrecht, Springer 2007, pp. 61-72.

F.R. Chaddad & C. Iliopoulos, “Control Rights, Governance and the Costs of Ownership in Agricultural Cooperatives”, 29 Agribusiness: An International Journal 1, 2013, pp. 3-22.

M.L. Cook, “The Future of U.S. Agricultural Cooperatives: A Neo-Institutional Approach”, 77 American Journal of Agricultural Economics, 1995, pp. 1153-1159.

M.L. Cook & M.J. Burress, “A Cooperative Lifecycle Framework”, Working Paper, Department of Agricultural and Applied Economics, Missouri, Columbia, USA, University of Missouri 2009.

M.L. Cook & F.R. Chaddad, “Redesigning Cooperative Boundaries: The Emergence of New Models”, 5 American Journal of Agricultural Economics, 2004, pp. 1249-1253.

M.L. Cook & C. Iliopoulos, “Beginning to Inform the Theory of the Cooperative Firm: Emergence of the New Generation Cooperative”, Finnish Journal of Business Economics, 1999, pp. 525-535.

M.L. Cook & C. Iliopoulos, “Ill-Defined Property Rights in Collective Action: The Case of US Agricultural Cooperatives”, in C. Menard, C. (ed.), Institutions, Contracts, and Organizations: Perspectives from New Institutional Economics, London, Edward Elgar 2000, pp. 335-348.

E.F. Fama, “Agency Problems and the Theory of the Firm”, 88 Journal of Political Economy, 1980, pp. 288-307.

E.F. Fama & M.C. Jensen, “Separation of Ownership and Control”, 26 Journal of Law and Economics, 1983, pp. 301-326.

M.E. Fulton & B. Hueth, “Cooperative Conversions, Failures and Restructurings: An Overview”, 23 Journal of Cooperatives, 2009, pp. i-xi.

A. Grandori, Organization and Economic Behavior, New York, Routledge 2001.

S.J. Grossman & O.D. Hart, “The Costs and Benefits of Ownership: A Theory of Vertical and Lateral Integration”, 94 Journal of Political Economy 4, 1986, pp. 691-719.

H. Hansmann, The Ownership of Enterprise, The Belknap Press of Harvard University Press 1996.

O. Hart, Firms, Contracts, and Financial Structure, Oxford, Oxford University Press 1995.

G.W.J. Hendrikse & G.P. Veerman, “Marketing Co-operatives: An Incomplete Contracting Perspective”, 52 Journal of Agricultural Economics 1, 2001, pp. 53-64.

C. Iliopoulos, “Stakeholder Participation in Co-operative Capital in Western Agricultural Co-operatives”, in C. Gijselinckx, L. Zhao & S. Novkovic (eds.), Co-operative Innovations in China and the West, Houndmills, Palgrave Macmillan 2014, pp. 81-97.

C. Iliopoulos, “Public Support for Agricultural Cooperatives: An Organizational Economics Approach”, 84 Annals of Public and Cooperative Economics 3, 2013, pp. 1-12.

C. Iliopoulos & M.L. Cook, “Property Rights Constraints in Producer-Owned Firms: Solutions as Prerequisites for Successful Collective Entrepreneurship”, Sixth International Conference on Economics and Management of Networks (EMnet), Agadir, Morocco, November 21-23, 2013.

C. Iliopoulos & G.W.J. Hendrikse, “Influence Costs in Agribusiness Cooperatives: Evidence from Case Studies”, 39 International Studies of Management & Organization 4, 2009, pp. 60-80.

C. Iliopoulos & V. Valentinov, “Opportunism in Agricultural Cooperatives in Greece”, 41 Outlook on Agriculture 1, 2012, pp. 15-19.

A. Keskinen, M. Aaltonen & E. Mitleton-Kelly, Organizational Complexity, FFRC Publications 6/2003, Turku, Finland, Finland Futures Research Centre, Turku School of Economics and Business Administration 2003.

L. Lamprinakis & M.E. Fulton, “Does Acquisition of a Cooperative Generate Profits for the Buyer? The Dairyworld Case”, 42 Agricultural Economics Supplement, 2011, pp. 89-100.

L.W. Lind, “Market Orientation of the Swedish Pork Sector: The Case of the Demutualization of Swedish Meats”, 49 Acta Universitatis Agriculturae Sueciae, Uppsala, Swedish University of Agricultural Sciences 2011.

P. Milgrom & J. Roberts, Economics, Organization & Management, Englewood Cliffs, NJ, Prentice-Hall 1992.

J. Nilsson, G.L.H. Svendsen & G.T. Svendsen, “Are Large and Complex Agricultural Cooperatives Losing Their Social Capital?”, 28 Agribusiness: An International Journal 2, 2012, pp. 187-204.

W.P. Rogerson, “Contractual Solutions to the Hold-Up Problem”, 4 The Review of Economic Studies 59, 1992, pp. 777-793.

L.F. Schrader, “Equity Capital and Restructuring of Cooperatives as Investor-Oriented Firms”, 4 Journal of Agricultural Cooperation, 1989, pp. 41-53.

J.M. Staatz, “A Game-Theoretic Analysis of Decisionmaking in Farmer Cooperatives”, in J. Royer (ed.), Cooperative Theory: New Approaches, ACS Service Report 18, USDA, Washington, DC, 1987, pp. 117-147.

P. Vitaliano, “Cooperative Enterprise: An Alternative Conceptual Basis for Analyzing a Complex Institution”, 65 American Journal of Agricultural Economics, 1983, pp. 1078-1083.

-

1 According to the World Co-operative Monitor of the International Co-operative Alliance (ICA), in 2012 the total turnover of 523 agricultural cooperatives in 30 countries was approximately $598.90 billion. The 2014 report where this information was derived from can be found at <https://dl.dropboxusercontent.com/u/24617037/QRcode/WCM2014.pdf>.

-

2 Bijman et al. 2012.

-

3 In plain English, this is often expressed, as ‘the co-op is a co-op is a co-op’.

-

4 See, for example, Iliopoulos & Cook 2013; Cook & Burress 2009 and Cook 1995.

-

5 See, for example, Chaddad & Cook 2004; Hendrikse & Veerman 2001 and Cook & Iliopoulos 1999.

-

6 Hansmann 1996.

-

7 Chaddad & Cook 2004.

-

8 Chaddad & Iliopoulos 2013.

-

9 Cook & Iliopoulos 2000.

-

10 For example, in achieving food security or renewable energy consumption goals.

-

11 Milgrom & Roberts 1992.

-

12 Grossman & Hart 1986.

-

13 A quasirent is “the difference between the value created by a resource in a particular relation with respect to the value created in its best alternative relation or use (rent), minus the cost of search for and transfer to these alternative relations” (Grandori 2001, p. 237).

-

14 The hold-up problem arises when two factors are present: (1) parties to a future transaction must make non-contractible relationship-specific investments before the transaction takes place and (2) the specific form of the optimal transaction (e.g. quality-level specifications, time of delivery, what quantity of units) cannot be determined with certainty beforehand. The hold-up problem is a situation where two parties may be able to work most efficiently by cooperating but refrain from doing so due to concerns that they may give the other party increased bargaining power and thereby reduce their own profits. When party A has made a prior commitment to a relationship with party B, the latter can ‘hold up’ the former for the value of that commitment. The hold-up problem leads to severe economic costs and might also lead to underinvestment (Rogerson 1992).

-

15 Hart 1995.

-

16 Fama & Jensen 1983.

-

17 Aghion & Tirole 1997, p. 2.

-

18 Milgrom & Roberts 1992.

-

19 Alchian & Demsetz 1972; Fama 1980 and Fama & Jensen 1983.

-

20 Alchian & Demsetz 1972.

-

21 Berle and Means 1932.

-

22 For example, an open corporation, notably the stock listed corporation.

-

23 Usually with a preset upper limit of votes per member.

-

24 Chaddad & Iliopoulos 2013.

-

25 Chaddad & Cook 2004.

-

26 The term ‘traditional cooperatives with vertical investments’ refers to traditional agricultural cooperatives that have invested in limited liability companies or other forms of strategic alliances as a means of entering other vertical stages of their food supply chains (e.g. production of value-added food items or agricultural inputs).

-

27 Cook & Chaddad 2004.

-

28 Ibid.

-

29 Ibid.

-

30 Ibid.

-

31 Ibid.

-

32 Ibid.

-

33 Chaddad & Cook 2004.

-

34 Cook & Burress 2009.

-

35 For example, in Finland and the Netherlands; see Iliopoulos 2014.

-

36 Iliopoulos 2014.

-

37 Chaddad & Cook 2007; Fulton & Hueth 2009; Lamprinakis & Fulton 2011; Lind 2011.

-

38 Bijman, Hendrikse & Van Oijen 2013.

-

39 Chaddad & Iliopoulos 2013.

-

40 Bijman, Hendrikse & Van Oijen 2013.

-

41 Bijman, Hendrikse & Van Oijen 2013.

-

42 Iliopoulos & Cook 2013.

-

43 See, for example, Cook 1995; Cook & Iliopoulos 2000.

-

44 Cook 1995.

-

45 See, for example, Hansmann 1996; Iliopoulos & Hendrikse 2009.

-

46 Cook 1995.

-

47 Cook & Iliopoulos 2000.

-

48 Iliopoulos and Cook 2013.

-

49 Cook & Burress 2009.

-

50 Hansmann 1996.

-

51 Iliopoulos & Hendrikse 2009.

-

52 Hansmann 1996.

-

53 Cook & Burress 2009.

-

54 For example, degree of the members’ interest heterogeneity.

-

55 Iliopoulos 2014.

-

56 That is, as opposed to patron preferences.

-

57 Iliopoulos & Cook 2013.

-

58 Cook & Iliopoulos 2000.

-

59 Staatz 1987.

-

60 The term ‘cooperative degeneration’ comes from the game theoretical literature and refers to any type of organizational decline; see Cook & Burress 2009.

-

61 Keskinen, Aaltonen & Mitleton-Kelly 2003.

-

62 See Iliopoulos & Valentinov 2012.

-

63 Hansmann 1996.

-

64 See, for example, Iliopoulos & Cook 2013; Chaddad & Cook 2004 and Vitaliano 1983.

-

65 ‘Optimum result’ in this context should be read as optimum from the members’ point of view.

-

66 See Chaddad & Iliopoulos 2013.

-

67 See Iliopoulos 2013.

-

68 See, for example, Lichbach 1996.

-

69 For example, by allowing proportional (according to volume of patronage) voting in the general assembly and adopting separate voting pools per product or geographic region.

-

70 In this paper, the term ‘membership heterogeneity’ refers primarily to heterogeneity of members’ interests and/or preferences.

-

71 Cook & Burress 2009.

-

72 Iliopoulos 2013.

-

73 Iliopoulos & Cook 2013.

The Dovenschmidt Quarterly |

|

| Article | Ownership, Governance and Related Trade-Offs in Agricultural Cooperatives |

| Keywords | investment constraints, collective decision-making, organizational complexity, agricultural cooperative, residual ownership rights |

| Authors | Constantine Iliopoulos |

| DOI | 10.5553/DQ/221199812014002004004 |

|

Show PDF Show fullscreen Abstract Author's information Statistics Citation |

| This article has been viewed times. |

| This article been downloaded 0 times. |

Constantine Iliopoulos, 'Ownership, Governance and Related Trade-Offs in Agricultural Cooperatives', (2014) The Dovenschmidt Quarterly 159-167

|

Agricultural cooperatives represent a key institutional arrangement in the world food and agriculture industries. Understanding these business organizations by adopting multi-disciplinary perspectives serves both scholarly and societal needs. This article addresses two issues: (1) how agricultural cooperatives choose from a plethora of ownership and governance features and (2) what are the main trade-offs cooperatives face in making these choices. Both issues have important implications for the efficiency of collective entrepreneurship organizations in food supply chains and thus for food nutrition security and food quality. The article proffers observations based on the extant literature and the author’s field experience. It is concluded that agricultural cooperatives choose ownership and governance features in an attempt to attract risk capital for investments while optimizing collective decision-making efficiency. The main trade-offs that cooperatives address while making these choices are between (1) investor mentality and member-patron control, (2) organizational complexity and vagueness of ownership rights, (3) the need for risk capital and member control, (4) organizational complexity and member control and (5) management monitoring costs and the costs of collective decision-making. These observations are highly relevant for organizational scholars, cooperative practitioners and policymakers as they inform decision-making in cooperatives in more than one way. |