-

1 Introduction

It is very common for parties involved in insolvency situations to perceive the value of a distressed company differently. Consider, for example, financiers who disagree with shareholders on the going-concern value of the company where a debt-for-equity swap, debt-write-off (‘haircut’) or other financial restructuring measures are proposed. Disagreements may also arise on the transfer of assets in a formal bankruptcy procedure in which an appointed administrator or liquidator attempts to negotiate the best deal for creditors by selling the bankrupt company, or pieces thereof, on a going-concern basis. Such divergent value perceptions are often a source of conflict.

In these conflicts, insolvency practitioners – a common name for lawyers, accountants and other experts who specialise in dealing with companies in financial distress – are confronted with complex valuation issues. Ideally, in evaluating business valuations and valuators, the judgments are based solely on the correct application of the relevant valuation method. However, business valuations are complex and technical exercises that require extensive experience and advanced quantitative and financial expertise. This then begs the question – on which grounds do insolvency practitioners (either as a representative of a stakeholder or as a representative of the court) evaluate valuators and their valuations, since most of them are not trained in this field?

This question is important for at least the following reason. The instances in which insolvency practitioners are confronted with valuation issues are expected to increase. In the context of (near) insolvency, for example, insolvency practitioners are already increasingly presented with complex valuation issues because of the global trend towards business rescue (rather than having businesses file for bankruptcy). Specifically, following the example of Chapter 11 proceedings in the US in which debt restructurings allow businesses to continue as a going concern, other countries are now adopting laws and regulations that aim to provide businesses with a second chance. For example, the UK has its so-called scheme of arrangements (Companies Act, 2006) in which the court arranges debt restructurings and forms agreements between shareholders and creditors with the goal of facilitating a fresh start. Similar procedures are found in, for example, Australia (Corporations Act, 2001) and South Africa (Companies Act, 2008). Likewise, the European Committee is actively working on harmonising its nation-states’ bankruptcy laws with the purpose of enabling business rescues to run more smoothly. In that spirit, The Netherlands introduced a rather sophisticated scheme of arrangement procedure in 2021, called the Act on the Confirmation of Private Restructuring Plans (ACPRP), or ‘Wet Homologatie Onderhands Akkoord’ in Dutch (WHOA). With this growing focus on business rescue, valuation issues are becoming increasingly common. For example, based on a valuation of a company’s earning capacity, bankruptcy judges must determine (to minimise damages for creditors) whether a business is more valuable as a going concern or whether its liquidation is more economical.

Given the inherent complexity of judging valuations on their own merit, we investigate which factors might unjustifiably influence insolvency practitioners’ judgments of valuators and their valuations. Specifically, we aim to explore whether cognitive biases can affect the trust that insolvency practitioners have in valuators and in the soundness of these valuators’ valuations. In this way, we seek to not only expand the existing literature on biases in judicial proceedings by examining cognitive biases in an insolvency and business valuation context, but, more importantly, to further our understanding of potential issues that might arise in the numerous cases where insolvency practitioners are confronted with (subjective) decision-making under uncertainty and ambiguity, for example, debtor-creditor negotiations, director liability assessments, management evaluations in debtor-in-possession procedures, or reorganisation plan examination.

In the following, we present our theoretical framework and introduce the concept of cognitive bias, for which we draw from the voluminous literature on biases in judicial decision-making. Next, we introduce our experimental study into the role of these biases in insolvency practice and later present a general discussion of the findings. -

2 Theoretical Background and Hypothesis Development

2.1 Biases in Legal Decision-Making

The notion that humans can deviate from the rational standard as a result of heuristics and biases has been well established1x E.g., A. Tversky and D. Kahneman, ‘Judgment Under Uncertainty: Heuristics and Biases’, 185(4157) Science 1124 (1974); D. Kahneman and A. Tversky, ‘Prospect Theory: An Analysis of Decision under Risk’, 47(2) Econometrica 263 (1979). and has also been extended to legal decision-making.2x E.g., C. Guthrie, J.J. Rachlinski & A.J. Wistrich, ‘Blinking on the Bench: How Judges Decide Cases’, 93 Cornell Law Review 1(2007). See also S.D. Franck et al., ‘Inside the Arbitrator’s Mind’, 66 Emory Law Journal 1115 (2017) for a study among arbitrators; also, N. Steblay et al., ‘The Impact on Juror Verdicts of Judicial Instruction to Disregard Inadmissible Evidence: A Meta-analysis’, 30 Law & Human Behavior 469 (2006) for a meta-analysis (of 75 hypotheses tests from 48 studies examining 8,474 participants) showing that judicial instructions to disregard inadmissible evidence impact verdicts in ways consistent with the content of the inadmissible evidence. For evidence on in-group bias, analysing 1,748 judicial decisions, see M. Shayo and A. Zussman, ‘Judicial Ingroup Bias in the Shadow of Terrorism’, 126(3) The Quarterly Journal of Economics 1447 (2011). For intervention strategies, see J. Kang et al., ‘Implicit Bias in the Courtroom’, 59 UCLA Law Review 1124 (2012). For a recent overview of the field, see J.J. Rachlinski and A.J. Wistrich, ‘Judging the Judiciary by the Numbers: Empirical Research on Judges’, 13 Annual Review of Law & Social Science 203 (2017). Indeed, over the past few decades, ample evidence has been gathered on how cognitive bias and intuitive thinking impact decision-making by legal decision-makers such as judges and jurors.3x For examples concerning discrimination and equal employment opportunity, hindsight bias and anchoring bias in tort law, and law-making, see L.H. Krieger, ‘The Content of Our Categories: A Cognitive Bias Approach to Discrimination and Equal Employment Opportunity’, 47(6) Stanford Law Review 1161 (1995); E.M. Harley, ‘Hindsight Bias in Legal Decision Making’, 25(1) Social Cognition 48 (2007); P.G. Peters Jr., ‘Hindsight Bias and Tort Liability: Avoiding Premature Conclusions’, 31(4) Arizona State Law Journal 1277 (2000); J.K. Robbennolt and C.A. Studebaker, ‘Anchoring in the Courtroom: The Effects of Caps on Punitive Damages’, 23(3) Law and Human Behavior 353 (1999); N. Strohmaier, H. Pluut, K. van den Bos, et al., ‘Hindsight Bias and Outcome Bias in Judging Directors’ Liability and the Role of Free Beliefs’, 51(3) Journal of Applied Social Psychology 141 (2021); W. Eskridge and J. Ferejohn, ‘Structuring Lawmaking to Reduce Cognitive Bias: A Critical View’, 87(2) Cornell Law Review 616 (2002). For example, in an seminal experiment with 167 federal magistrate judges, Guthrie, Rachlinski and Wistrich examined five biases (i.e. anchoring effect, framing effect, hindsight bias, representativeness heuristic, egocentric bias) and found that each of these impacts judicial decision-making.4x C. Guthrie, J.J. Rachlinski & A.J. Wistrich, ‘Inside the Judicial Mind’, 86 Cornell Law Review 777 (2001). They extended these findings to administrative law judges (ALJ) in separate work and found that ALJs “tend to make ordinary judgments in a predominantly intuitive way”.5x C. Guthrie, J.J. Rachlinski & A. J. Wistrich, ‘The “Hidden Judiciary”: An Empirical Examination of Executive Branch Justice’. 58 Duke Law Journal 1477-1530 (2009).

The notion that intuition and extra-legal factors can play a role in legal decision-making and thus that it not necessarily follows the typically prescribed formalistic model – one in which judges merely apply the relevant laws to the facts of a case in a mechanistic fashion – is widely recognised. For example, in their theory of juror decision-making, Pennington and Hastie propose story construction as the central cognitive process in juror decision-making.6x N. Pennington and R. Hastie, ‘A Cognitive Theory of Juror Decision Making: The Story Model’, 13 Cardozo Law Review 519 (1991). See also M. Vorms and D. Lagnado, ‘Coherence and Credibility in the Story-Model of Jurors’ Decision-Making: Does Mental Simulation Really Drive the Evaluation of the Evidence?’ 49 Studies in Applied Philosophy, Epistemology and Rational Ethics 103 (2019). Jurors choose from various stories (i.e. narrative summaries of events under dispute) the most coherent (i.e. consistent-plausible-complete) story, after which they reach a verdict if the accepted story fits a verdict category as instructed by the judge. According to their story model, extra-legal factors are most likely to enter the decision-making when there is little information on which a narrative can be based or when the extra-legal information is consistent with the constructive narrative.

The story model displays similarities with an alternative model developed by Simon, which aims to reconcile the rationalist/formalistic models and the critical models (with their roots in legal realism) and recognises as well the processes that deviate from the formalistic ‘ideal’. Simon’s cognitive coherence-based reasoning model has as its starting point the notion that people are generally cognitively lazy and that the mind therefore aims to transform complex decision-making tasks into more simple ones, such that stronger, more confident conclusions can be reached.7x D. Simon, ‘A Third View of the Black Box: Cognitive Coherence in Legal Decision Making’. 71 University of Chicago Law Review 511-86 (2004). The model suggests that people shift between rationalist and intuitive modes of reasoning and that these two modes interact in such a way that the presented facts and legal rules drive our intuitive sense-making process, but also that our formed intuitions and preferred conclusions subsequently influence our reconstruction of case facts and legal rules, thus creating a bidirectional mechanism between reason and intuition.

In summary, consensus exists regarding the idea that legal decision-making is not necessarily a logical and rule-bound process based on deductive reasoning, as legal formalists claim. Complex psychological mechanisms are involved in which unconscious systematic errors (i.e. cognitive bias) can exert considerable influence on legal decision-making.8x L.J. Curley, J. Munro & I.E. Dror, ‘Cognitive and Human Factors in Legal Layperson Decision Making: Sources of Bias in Juror Decision Making’, 62(3) Medicine, Science, and the Law 206 (2022).

In addition to biases in legal decision-making, biases in financial decision-making have also received ample research attention.9x E.g., B.N. Adebambo & X. Yan, ‘Investor Overconfidence, Firm Valuation, and Corporate Decisions’, 64(11) Management Science 5349 (2018); M. Baker, R. Ruback & J. Wurgler, ‘Behavioral Corporate Finance’, in B.E. Eckbo (ed.), Handbook of Corporate Finance: Empirical Corporate Finance (2007); I. Ben-David, J.R. Graham & C.R. Harvey, ‘Managerial Overconfidence and Corporate Policies’, NBER Working Paper Series (2007); E. Bikas, D. Jurevičienė, P. Dubinskas, et al., ‘Behavorial Finance: The Emergence and Development Trends’, 82 Procedia – Social and Behavorial Sciences 870 (2013); K. Daniel, D. Hirshleifer & A. Subrahmanyam, ‘Investor Psychology and Security Market Under- and Overreactions’, 53(6) Journal of Finance 1839 (1998); W.F.M. de Bondt and R.H. Thaler, ‘Financial Decision Making in Markets and Firms: A Behavorial Perspective’, in R. Jarrow, V. Maksimovic & W.T. Ziemba (eds.), Handbooks in Operations Research and Management Science (1995) 385; J.B. Heaton, ‘Managerial Optimism and Corporate Finance’, 31(2) Financial Management 33 (2002); R. Roll, ‘The Hubris Hypothesis of Corporate Takeovers’, 59(2) The Journal of Business 197 (1986); H. Shefrin and M. Statman, ‘The Disposition to Sell Winners Too Early and Ride Losers Too Long: Theory and Evidence’, 40(3) The Journal of Finance 777 (1985); R.J. Shiller, ‘From Efficient Markets Theory to Behavorial Finance’, 17(1) Journal of Economic Perspectives 83 (2003); P. Slovic, ‘Psychological Study of Human Judgment: Implications for Investment Decision Making’, 27(4) The Journal of Finance 779 (1972). For example, in the context of investments, overconfidence of investors typically results in overvaluing a particular firm.10x B. Nikolic and X. Yan, ‘Investor Overconfidence, Misvaluation, and Corporate Decisions’, 2(1) Journal of Financial Economics 52 (2014). In the context of personal bankruptcy proceedings, anchoring effects were found inasmuch that courts rarely deviate from the debtor’s payment plan as recommended in the official receiver’s financial report, which provides the main facts and a recommendation for the court’s final decision.11x Y. Mugerman, N. Neta & O. Moran, ‘Are Courts Biased? The Anchoring Heuristic and Judicial Decisions in Personal Bankruptcy Proceedings’, in I. Venezia (ed.), Behavioral Finance: A Novel Approach. (2020), 99-128. However, to our knowledge, little research has been done on the cross-section of the two fields covered in the present article – law and finance – and no empirical research has yet investigated how biases might affect insolvency practitioners in the context of disputes involving business valuations. We consider this gap important to fill, as further insights into the dynamics of decision-making by insolvency practitioners increase legal certainty and fairness. Moreover, insights into biases affecting insolvency practitioners when dealing with valuation issues can possibly help these professionals avoid the unnecessary loss of social and economic value – including loss of employment – when viable business activities are liquidated that could have been saved.12x Considering the current developments in the field of AI, a relevant question becomes as to what extent AI may assist (or one day replace) insolvency practitioners in dealing with valuation issues or assist or replace valuators in conducting valuations. However, even if AI would assist in business valuation conflict situations, as AI may do better in statistical prediction and risk assessment – e.g., see C.R. Sunstein, ‘Governing by Algorithm? No Noise and (Potentially) Less Bias’, 71(6) Duke Law Journal 1175 (2022), or C. McKay, ‘Predicting Risk in Criminal Procedure: Actuarial Tools, Algorithms, AI and Judicial Decision-Making’, 32(1) Current Issues in Criminal Justice 22 (2020) – it will still be a long time before bias-free judicial decision-making becomes a reality. Whereas in the view of Carl Sunstein – see C.R. Sunstein, ‘Algorithms, Correcting Biases’, 86(2) Social Research: An International Quarterly 499 (2019) – algorithms do much better than real-world judges in various court decision contexts, and there is evidence that AI contains cognitive bias or that cognitive biases hold advantages for AI (e.g. effort reduction, speed). For evidence that AI contains cognitive bias, see e.g., M. Abudy, I. Gildin & Y. Mugerman, ‘Do Computerized Traders Follow Social Norms? Evidence from the Holocaust Remembrance Moment of Silence’, 48 Finance Research Letters 102914 (2022). For the advantages of cognitive biases for AI, see T. Hagendorff and S. Fabi, ‘Why We Need Biased AI: How Including Cognitive Bias Can Enhance AI systems’, Journal of Experimental & Theoretical Artificial Intelligence, online first (2023).Having described the general context of the present research, we now turn to a brief discussion of the relevant literature regarding the specific biases that are the focus of the experiment discussed below, and we also introduce our hypotheses for the biases.

2.2 Similarity Bias

Similarity bias is usually conceptualised as prejudice towards and a biased perception of another individual based on sharing certain traits with that individual, such that those who are perceived to be more similar are evaluated more positively.13x E.g., D.E. Byrne, ‘The Attraction Paradigm’, 3(2) Behavior Therapy 337 (1972); C.H. Vivian Chen, H.M. Lee & Y.J. Yvonne Yeh, ‘The Antecedent and Consequence of Person-Organization Fit: Ingratiation, Similarity, Hiring Recommendations and Job Offer’, 16(3) International Journal of Selection and Assessment 210 (2008). Similarity bias has been shown to affect perceptions and judgments across a wide range of contexts, such as performance evaluations,14x E.g., D.B. Turban and A.E. Jones, ‘Supervisor-Subordinate Similarity: Types, Effects and Mechanisms’, 73(2) Journal of Applied Psychology 228 (1988). hiring decisions15x E.g., Vivian Chen et al., above n. 13. and cooperative behaviour.16x E.g., D. Balliet, J. Wu & C.K.W. de Dreu, ‘Ingroup Favoritism in Cooperation: A Meta-analysis’, 140(6) Psychological Bulletin 1556 (2014).

Most important for the present purposes, similarity biases have also been found in legal decision-making. For example, it has been shown that minority participants (acting as jury members) showed positive in-group biases when evaluating the culpability of rape offenders, such that perpetrators were more often judged to be guilty when the rape victim was of the same ethnicity as the participant.17x N.A. Rector and R.M. Bagby, ‘Minority Juridic Decision Making’, 36(1) British Journal of Social Psychology 69 (1997). Moreover, jury members who saw themselves as similar to the defendant in terms of religiosity were typically less certain of the defendant’s culpability.18x M.K. Miller, J. Maskaly, M. Green, et al., ‘The Effects of Deliberations and Religious Identity on Mock Jurors’ Verdicts’, 14(4) Group Processes and Intergroup Relations 517 (2011). Also, mock jury members perceived an expert witness as more credible when they also perceived the expert witness to be more similar to themselves in terms of personality.19x B.O. Gardner, C. Titcomb, R.J. Cramer, et al., ‘Perceived Personality Similarity and Perceptions of Expert Testimony’, 34(4) Journal of Individual Differences 185 (2013). Importantly, these effects seem not to be limited to lay people (i.e. jury members); they appear to affect legal practitioners as well. Specifically, it has been found that justices’ votes in the US Supreme Court freedom-of-expression cases reflected their personal preferences towards the speech’s ideological grouping (i.e. conservative or liberal), concluding that the US Supreme Court judges can be affected by in-group biases.20x L. Epstein, C.M. Parker & J.A. Segal, ‘Do Justices Defend the Speech They Hate? An Analysis of In-Group Bias on the US Supreme Court’, 6(2) Journal of Law and Courts 237 (2018). See also M. Shayo and A. Zussman, ‘Judicial Ingroup Bias in the Shadow of Terrorism’, 126(3) The Quarterly Journal of Economics 1447 (2011).

However, it remains uncertain whether similarity bias can affect insolvency practitioners when dealing with business valuation matters, especially because the evidence of similarity bias in financial decision-making is scarce. Nonetheless, some research suggests financial judgments are not immune to similarity bias. For example, venture capitalists have been shown to evaluate opportunities more favourably when these are represented by entrepreneurs who ‘think’ in ways similar to their own and that they tend to favour teams similar to themselves in type of training and experience.21x N. Franke, M. Gruber, D. Harhoff, et al., ‘What You Are Is What You Like – Similarity Biases In Venture Capitalists’ Evaluations of Start-up Teams’, 21(6) Journal of Business Venturing 802 (2006); C.Y. Murnieks, J.M. Haynie, R.E. Wiltbank, et al., “I Like How You Think”: Similarity as an Interaction Bias in the Investor-Entrepreneur Dyad’, 48(7) Journal of Management Studies 1533 (2011). Also, recent work has shown that when financial analysts perceive a CEO to be similar to themselves in terms of personality, they will issue more positive forecasts of the CEO’s company than when they perceive the CEO to be dissimilar22x J. Becker, J. Medjedovic & C. Merkle, ‘The Effect of CEO Extraversion on Analyst Forecasts: Stereotypes and Similarity Bias’, 54(1) The Financial Review 133 (2019).

We consider it an interesting and relevant question to test empirically whether insolvency practitioners are affected by similarity bias when judging valuators and their work. Could it be, for example, that insolvency practitioners have more trust in a valuation made by a valuator who they perceive as similar to themselves, even though this valuation might actually be of lesser quality than one conducted by a valuator who they perceive as less similar? To examine the potential existence of such a similarity bias, we formulated the following hypothesis:H1a: When insolvency practitioners perceive a valuator to be more similar to themselves, they have more trust in the valuation.

In addition to testing the hypothesised link between perceived similarity and trust in a valuation, we are also interested in the extent to which perceived trustworthiness of the valuator mediates this relationship. We expect that the higher the similarity between an insolvency professional and a valuator, the more trustworthy the valuator will be perceived to be and, consequently, the more trust the insolvency professional will have in the valuator’s valuation.

The distinction between trust and trustworthiness deserves further consideration. The act of trusting a valuation outcome and using that outcome in subsequent negotiations is considered an act of trust, as trust can be defined as the willingness to take a risk in a relationship or as “a psychological state comprising the intention to accept vulnerability based upon positive expectations of the intentions or behaviour of another”.23x R.C. Mayer, J.H. Davis & F.D. Schoorman, ‘An Integrative Model of Organizational Trust’, 20(3) The Academy of Management Review 709 (1995). See also D.M. Rousseau, S.B. Sitkin, R.S. Burt, et al., ‘Not So Different after All: A Cross-Discipline View of Trust’, 23(3) The Academy of Management Review 393 (1998). Trustworthiness is different in that it is a quality of a particular person rather than an action. An insolvency professional who considers a valuator to be trustworthy believes that valuator is competent, benevolent and honest, which together lead to heightened trust in the valuator.24x Mayer et al., above n. 23. Hence, we expect perceived trustworthiness of a valuator to mediate the relationship between perceived similarity and trust in the valuator’s valuation.

There is evidence for the notion that perceptions of trustworthiness can be affected by the degree a person is perceived as similar by an observer.25x E.g., J.A. Cazier, B.B.M. Shao & R.D. St. Louis, ‘Sharing Information and Building Trust through Value Congruence’, 9(5) Information Systems Frontiers 515 (2007); S.S. Lui, H.Y. Ngo & A.H.Y. Hon, ‘Coercive Strategy in Interfirm Cooperation: Mediating Roles of Interpersonal and Interorganizational Trust’, 59(4) Journal of Business Research 466 (2006); P. Racherla, M. Mandiviwalla & D.J. Connolly, ‘Factors Affecting Consumers’ Trust in Online Product Reviews’, 11(2) Journal of Consumer Behaviour 94 (2012); H.E. Yildiz, ‘“Us vs. Them” or “Us over Them”? On the Roles of Similarity and Status in M&As’, 25(1) International Business Review 51 (2015). For example, even when people only match in terms of facial features, this is sufficient to increase perceptions of trustworthiness,26x L.M. DeBruine, ‘Trustworthy but Not Lust-Worthy: Context-specific Effects of Facial Resemblance’, 272(1566) Proceedings of the Royal Society B: Biological Sciences 919 (2005); H. Farmer, R. McKay & M. Tsakiris, ‘Trust in Me: Trustworthy Others Are Seen as More Physically Similar to the Self’, 25(1) Psychological Science 290 (2014). as well as subsequent cooperation.27x L.M. DeBruine, ‘Facial Resemblance Enhances Trust’, 269(1498) Proceeding of the Royal Society B: Biological Sciences 1307 (2002); M.E. Kret, A.H. Fischer & C.K.W. de Dreu, ‘Pupil Mimicry Correlates with Trust in In-group Partners with Dilating Pupils’, 26(9) Psychological Science 1401 (2015); D.B. Krupp, L.M. DeBruine & P. Barclay, ‘A Cue of Kinship Promotes Cooperation for the Public Good’, 29(1) Evolution and Human Behavior 49 (2008). Therefore, based on the above we formulated the following hypothesis:H1b: Perceived trustworthiness of the valuator mediates the relationship between perceived similarity and trust in the valuation.

2.3 Outcome Bias

Outcome bias is the tendency to take the outcome of a certain decision into account when evaluating that decision, “in a way that is irrelevant to the true quality of the decision”.28x J. Baron and J.C. Hershey, ‘Outcome Bias in Decision Evaluation’, 54(4) Journal of Personality and Social Psychology 569, at 570 (1988). In other words, people tend to judge the quality of an earlier decision for a large part on its outcome rather than on evaluating the elements that led to the decision.

A substantive body of literature has been published on outcome bias across a range of different contexts. For example, in a medical context it has been demonstrated that when people are asked to evaluate a surgeon’s decision to perform an operation on a patient, this decision is judged more negatively when (all else being equal) the operation ultimately fails and the patient dies, compared to when the operation is successful and the patient recovers.29x O. Sezer, T. Zhang, F. Gino, et al., ‘Overcoming the Outcome Bias: Making Intentions Matter’, 137 Organizational Behavior and Human Decision Processes 13 (2016). In financial decision-making, people believed an auditor to be more negligent after an adverse outcome (i.e. business failure) compared to when these individuals remained ignorant of the outcome.30x K. Kadous, ‘The Effects of Audit Quality and Consequence Severity on Juror Evaluations of Auditor Responsibility for Plaintiff Losses’, 75(3) The Accounting Review 327; M.E. Peecher and M.D. Piercey, ‘Judging Audit Quality in Light of Adverse Outcomes: Evidence of Outcome Bias and Reverse Outcome Bias’, 25(1) Contemporary Accounting 243 (2008). Also, when finance managers had to evaluate their agents’ investment strategies and assign bonuses accordingly, these managers evaluated the same strategy more favourably when it resulted in a good payoff, even if they otherwise had a negative perception of the investment strategy.31x C. Köning-Kersting, M. Pollmann, J. Potters, et al., ‘Good Decision vs. Good Results: Outcome Bias in Financial Agents’ Rewards’, Working Paper 2017.

Outcome biases can also be found in legal decision-making. For example, evaluations of medical negligence were strongly influenced by the knowledge of an adverse outcome, such that the same actions of a medical specialist were evaluated less harshly if one was ignorant of any adverse outcome.32x T.B. Hugh and S.W.A. Dekker, ‘Hindsight Bias and Outcome Bias in the Social Construction of Medical Negligence: A Review’, 16(5) Journal of Law and Medicine 846 (2009); see also Harley, above n. 3; K.A. Kamin and J.J. Rachlinski, ‘Ex Post ≠ Ex ante: Determining Liability in Hindsight’, 19(1) Law and Human Behavior 89 (1995). There is also some evidence that legal professionals such as judges can be affected by outcome information.33x E.g., J.C. Anderson, D.J. Lowe & P.M.J. Reckers, ‘Evaluation of Auditor Decisions: Hindsight Bias Effects and the Expectation Gap’, 14(4) Journal of Economic Psychology 711 (1993); M. Kneer and S. Bourgeois-Gironde, ‘Mens rea Ascription, Expertise and Outcome Effects: Professional Judges Surveyed’, 169 Cognition 139 (2017).

We investigate whether insolvency practitioners are affected by outcome information when evaluating a business valuator. Specifically, when a business valuator conducts a valuation and this valuation is used to negotiate a deal, will insolvency practitioners evaluate the valuator more negatively when the deal turns out to be a bad one compared to when the deal turns out to be a good one? Outcome bias can be disadvantageous for valuators as this may result in increasingly negative perceptions of both the valuation and the valuator when the outcome of a deal is unfavourable. Hence, valuators might be exposed to the risk of being unduly blamed for an adverse outcome, being excluded from future work despite the quality and soundness of their work or even held liable. The problem for insolvency practitioners could be that they might engage valuators in new cases who are perhaps less experienced or specialised, as a result of which both the quality of the valuation could be at risk and chances of a successful business rescue might diminish as well. To test whether insolvency practitioners are affected by outcome bias in this context, we formulated the following hypothesis:H2: Valuators will be judged more negatively following an undesirable outcome and more positively following a desirable outcome.

2.4. Gender Bias

Gender bias can be described as a predilection or predisposition towards one gender over the other. The bias can be conscious or unconscious, and may be visible in many ways, either subtly or obviously.34x C.L. Ridgeway, ‘Gender, Status, and Leadership’, 57(4) Journal of Social Issues 637 (2001). There are quite a few studies available showing gender bias in a legal context, specifically studies demonstrating that men favour other men.35x S. Hodgson and B. Pryor, ‘Sex Discrimination in the Courtroom: Attorney’s Gender and Credibility’, 55(2) Psychological Reports 483 (1984); J. Resnik, ‘Gender Bias: From Classes to Courts’, 45(6) Stanford Law Review 2195 (1993); J. Yourstone, T. Lindholm, M. Grann, et al., ‘Evidence of Gender Bias in Legal Insanity Evaluations: A Case Vignette Study of Clinicians, Judges and Students’, 62(4) Nordic Journal of Psychiatry 273 (2008); see further, e.g., M. Fay and L. Williams, ‘Gender Bias and the Availability of Business Loans’, 8(4) Journal of Business Venturing 363 (1993); L. Macnell, A. Driscoll & A.N. Hunt, ‘What’s in a Name: Exposing Gender Bias in Student Ratings of Teaching’, 40(4) Innovative Higher Education 291 (2015); C.M. Marlowe, S.L. Schneider & C.E. Nelson, ‘Gender and Attractiveness Biases in Hiring Decisions: Are More Experiences Managers Less Biased?’, 81(1) Journal of Applied Psychology 11 (1996); C.A. Moss-Racusin, J.F. Dovidio, V.L. Brescoll, et al., ‘Science Faculty’s Subtle Gender Biases Favor Male Students’, 109(41) Proceedings of the National Academy of Sciences of the United States of America 16474 (2012). There are also research findings that demonstrate that men typically have more trust in other men’s expertise and generally consider men to be more knowledgeable and skilful than women.36x E.g., M.E. Heilman & M.C. Haynes, ‘No Credit Where Credit Is Due: Attributional Rationalization of Women’s Success in Male–Female Teams’, 90(5) Journal of Applied Psychology 905 (2005); J. Swim, ‘He’s Skilled, She’s Lucky: A Meta-Analysis of Observers’ Attributions for Women’s and Men’s Successes and Failures’, 22(5) Personality and Social Psychology Bulletin 507 (1996); M.C. Thomas-Hunt & K.W. Phillips, ‘When What You Know Is Not Enough: Expertise and Gender Dynamics in Task Groups’, 30(12) Personality & Social Psychology Bulletin 1585 (2004). Conversely, there is some research available showing that women are harsher when judging men.37x E.g., E.E. Johansson, G. Risberg, K. Hamberg, et al., ‘Gender Bias in Female Physician Assessments: Women Considered Better Suited for Qualitative Research’, 20(2) Scandinavian Journal of Primary Health Care 79 (2002). Interestingly, based on the foregoing, it appears that it is not only men who judge women more negatively; in some contexts, women judge other women more negatively as well, whereas in other contexts they are perceived more positively. Indeed, gender bias is not consistently found among men and women and differs inasmuch that people sometimes favour their own gender and at other times the other gender. Therefore, it is not completely clear how gender bias might affect perceptions of insolvency practitioners on valuators and their valuations. Another reason to be unsure about the existence of gender bias in this context is the ambiguity of the intensity and persistence of gender bias. On the one hand, research shows there is evidence of changing attitudes towards, for example, both female and male leaders, and, on the other, a significant proportion of men and women judging their leaders still prefer male leaders over female leaders.38x A. Eagly and S.J. Karau, ‘Role Congruity Theory of Prejudice toward Female Leaders’, 109(3) Psychological Review 573 (2002); K. Elsesser & J. Lever, ‘Does Gender Bias Against Female Leaders Persist? Quantitative and Qualitative Data from a Large-scale Survey’, 64(12) Human Relations 1555 (2011).

Based on the above, we are unsure whether gender bias plays a prominent role in how insolvency practitioners perceive experts like valuators and, consequently, their valuations. Any influence of gender bias is probably disadvantageous for valuators as this may possibly affect perceived trustworthiness. Due to the existence of gender bias, valuators and/or other practitioners active in the insolvency industry may be at risk of being perceived as incompetent or less capable based on their gender and even be excluded from future work despite the quality and soundness of their work. However, given the mixed findings of gender bias in the literature and uncertainty regarding changes in attitudes towards men and women in the present-day society, we do not formulate a hypothesis for this bias in this study and consider our analyses pertaining to gender bias to be exploratory in nature. -

3 Method

3.1 Participants

A total of 272 insolvency practitioners in the field of business rescue and insolvency completed an online survey for which they were approached via e-mail. Participants were members of INSOL International, a worldwide federation of legal and financial experts who specialise in dealing with companies in financial distress.39x Roughly 3,000 professionals were approached via e-mail to participate in the survey. As we did not know with certainty whether all available contact details were up to date, we cannot establish with certainty what the response rate is. Assuming that 10% to 20% of the details were incorrect, the response rate is slightly above 10%. INSOL International has 10,500 members worldwide (see https://www.insol.org/fellows/). Data collection took place in 2019 and was completed in a single round (with one reminder e-mail). No one who was contacted via e-mail replied to decline participation. To ensure a relevant sample was obtained for our purposes, participants were asked whether they are confronted with decisions in their work that involve valuation outcomes; 83.5% answered positively.40x The results do not differ significantly when only this group is analysed.

We aimed to get an even split between male and female participants, resulting in a distribution of 126 women (46.3%) and 146 men. The average age of the participants was 45.1 years (SD = 11.5), and they had on average 19.1 years (SD = 11.2) of professional experience.41x SD = Standard Deviation. As many as 40 different countries are represented in the sample. The six most represented countries are: UK (26.5%), Australia (16.2%), South Africa (9.2%), Canada (5.5%), USA (4.8%) and the Netherlands (4.8%).3.2 Design and Procedure

The vignette experiment consisted of two consecutive parts.42x Vignette studies are widely used to examine decision-making processes. See e.g., J.R. Brown et al., ‘Behavioral Impediments to Valuing Annuities: Complexity and Choice Bracketing’, 103(3) The Review of Economics and Statistics 533 (2021), or S.C. Evans et al., ‘Vignette Methodologies for Studying Clinicians’ Decision-Making: Validity, Utility, and Application in ICD-11 Field Studies’, 15(2) International Journal of Clinical and Health Psychology 160 (2015). For an overview paper on best practices concerning experimental vignette studies, see H. Aguinis & K.J. Bradley, ‘Best Practice Recommendations for Designing and Implementing Experimental Vignette Methodology Studies’. 17(4) Organizational Research Methods 351-71 (2014). In the first part, participants were presented with the first part of the business case concerning a business that recently went bankrupt and for which a trustee was appointed to settle the estate. In the case, the trustee hired a valuator to determine the value of the company prior to engaging in negotiations with potential buyers. Participants were asked to put themselves in the shoes of the appointed trustee and to evaluate the valuation and role of the valuator from the perspective of the trustee handling the estate. For half of the participants, the description of the valuator matched the participant in key aspects (i.e. high-similarity condition), whereas for the other half the description mismatched the participant (i.e. low-similarity condition). After reading the first part of the case, participants were presented with three questions that aimed to measure the participants’ perceived similarity with the valuator. Next, three questions were presented to measure the perceived trustworthiness of the valuator. Finally, participants were asked to answer four questions that measured the participants’ trust in the valuation itself.

In the second part of the experiment, participants were presented with the outcome of the case, in which a deal was closed with a buyer of the entire estate. Half of the participants received an outcome in which the deal turned out to be very good, and the other half were presented with an outcome detailing a bad deal. Next, participants were asked questions aimed at capturing the participants’ perception of the valuator’s role in bringing about a good deal or a bad deal. Thus, the first part of the experiment aimed to investigate the potential role of similarity bias in the evaluations of valuations and the second part of the experiment aimed to investigate the potential role of outcome bias in the evaluations of valuators.

At the end of the experiment, participants were asked whether English was their native language (68.0% indicated ‘yes’) and, if not, to what extent they properly understood the case and subsequent questions. Participants answered on a 7-point Likert scale ranging from (1) ‘Strongly disagree’ to (7) ‘Strongly agree’ (M = 6.52, SD = 0.68).43x M = Mean. Participants were debriefed and given the opportunity to provide feedback and leave behind their e-mail address, so they could be informed on the results of the study.44x We report all manipulations, all data exclusions and all measures in our study, so we note that two short sets of questions (10 in total) on free will and quality of sleep, and six general questions unrelated to the case on valuation practices in general were excluded from the analyses. These questions were pilot questions for a different research project. The results are available on request.

The key variables of interest in the first part of the experiment were the participants’ (1) trust in the valuation and (2) perception of the trustworthiness of the valuator, whereas in the second part this was the participants’ (3) evaluation of the role that the valuator played in bringing about the outcome of the deal.3.3 Part 1 of the Case: Similarity and Firm Profile Manipulation

3.3.1 Case Description

The case description (fictitious, albeit based on a real-world case) as presented to the participants is provided here below.

History

Recently, one of UK’s respectable fashion companies, ‘International Women Clothing’ (‘the Company’), went bankrupt. Exceeding an annual turnover of GBP 100 million and having more than 350 people employed, the Company was unable to become profitable during the last years, partly due to a decline in consumer spending. After many years of different retrenchment programs and financial restructurings, no meaningful improvements became visible. In the last year the loss exceeded an amount of GBP 12 million. The banks and financiers of the Company decided to end the funding. A bankruptcy was inevitable after being in the market for more than twenty years.

Current situation

We would like you [the survey participant] to put yourself in the shoes of the trustee who is appointed by the court and whose main task is to optimize the revenues in the interest of the creditors. There is a potential candidate to relaunch the Company and that offers a serious chance for continuation of the Company (i.e., by means of a transfer of all assets of the bankrupt Company including most of its personnel). The most important assets are tradenames, distribution rights, inventory, software, and leases of prime properties.

The secured and unsecured creditors of the Company are exposed to a deficit of approx. GBP 25 million, including all costs to settle the estate. You strive to sell the assets of the bankrupt Company for at least this amount to minimize any shortage of the estate. By doing so, you may possibly satisfy all creditors. All Company’s stakeholders are of the opinion that these sales proceeds of the assets are realistic to expect. Importantly, outsiders follow the results in this bankruptcy with great interest as the (former) statutory director and main shareholder of the Company is well introduced in high society.

The potential buyer of the assets of the Company is a well-known European private equity firm (‘PE-firm’) specialized in fashion retail through one of its funds, but above all experienced in turnarounds of distressed companies. To prepare the negotiations with this potential buyer, you need some advice on the estimated value of the assets. Indeed, private equity is known for its financial knowledge and you want to avoid selling the assets too low. To realize a quick deal, you start the negotiations with this potential buyer who you know has the required capital to buy the assets. You hire a valuation professional who provides support in this delicate matter. Although the available budget for this work is limited as it increases the costs of the estate, it may eventually support in maximizing the sales proceeds.About the valuation professional and the valuation firm

You are introduced to a valuator called [Laura/Andrew] Matthews.45x Either the name Laura or Andrew, the identifiers/attributes ‘his or her, twenties or thirties or forties or fifties or sixties’, were added, respectively, depending on the experimental condition. [Laura/Andrew] Matthews is in [her/his] [twenties/thirties/forties/fifties/sixties] and is a certified valuation analyst accredited by the Association of Certified Business Valuators in the UK. [Laura/Andrew] has a BA in economics with a specialization in business valuation and has worked in different capacities in finance. For quite some years now [she/he] is active as a professional business valuator. [Laura/Andrew] Matthews works for [a/an] [small, local valuation/international Big Four] firm.46x Either a small, local valuation firm, or an international Big Four firm, was presented, as participants may base their trust in the valuator on the reputation of the valuator’s firm. To be able to account for the potential influence of the valuation firm’s reputation, we varied the size of the firm across participants.

Valuation

[Laura/Andrew] Matthews performed the valuation and presents the report, explaining the applied valuation assumptions and corresponding calculations in detail. A Discounted Cash Flow method (DCF, i.e. an intrinsic valuation) was used to calculate the present value of the future cash flows, applying an appropriate discount rate. The content of the valuation report includes the following main topics:

About the DCF-method

Historical performance

Return on capital, Reinvestment rate and Growth rate

Cash flow (from assets) projection

Discount rate

DCF-value of the assets (reflecting cash flow, growth, risk)

Unfortunately, it appears that the assets are valued at (rounded) GBP 18 million, around GBP 7 million less than the creditors deficit. Although a potential sale of GBP 18 million would imply a (mean) recovery rate of around 72%, senior unsecured and senior subordinated bond holders will lose a lot of money, contrary to earlier expectations.

The conclusion of the valuator is that based on the assumptions described in the report, the value of the assets at valuation date is GBP 18.25 million. Based on this outcome, a sale of the assets will very likely result in a deficit of the estate. Moreover, in the negotiations with the potential buyer it will now become more difficult to achieve sales proceeds close to GBP 25 million as they will probably do their math as well.

3.3.2 Measures

Actual similarity. As we measured the participant’s gender and age, we could match (high-similarity condition) or mismatch (low-similarity condition) the background information of the valuator that was given in the case. Specifically, for those in the high-similarity condition, the described valuator was of the same gender as the participant (i.e. Laura Matthews in case of a female participant and Andrew Matthews in case of a male participant) and of the same age (i.e. ‘in his/her thirties if the participant was between 30-39 years old’, ‘in his/her forties if the participant was between 40-49 years old’ etc.). In the low-similarity condition, the gender of the valuator was the opposite from the participant’s and the valuator’s age was as far away from the participant’s age as possible. If the participant was younger than 45, the case stated that the valuator was ‘in his/her sixties’, and if the participant was 45 years or older, the valuator was ‘in his late-twenties’. The details on valuator’s educational and professional background were kept consistent across the two conditions.

Perceived similarity. In addition to manipulating similarity by altering the profile of the valuator, we also measured perceived similarity with the valuator. This was done for two reasons. First, this allowed us to check whether the manipulation of similarity was successful, as this would mean the perceived similarity would be significantly higher in the high-similarity condition than in the low-similarity condition. Second, we wanted to examine the effect of both the actual (i.e. manipulated) similarity and the perceived similarity on trust in the valuation through its effects on perceived trustworthiness of the valuator. Previous research has shown that perceived similarity is typically a much stronger predictor of attitudes and behaviour than actual similarity.47x E.g., G.R. Ferris & T.A. Judge, ‘Personnel/Human Resources Management: A Political Influence Perspective’, 17(2) Journal of Management 447 (1991); J.P. Strauss, M.R. Barrick & M.L. Connerly, ‘An Investigation of Personality Similarity Effects (Relational and Perceived) on Peer and Supervisor Ratings and the Role of Familiarity And Liking’, 74(5) Journal of Occupational and Organizational Psychology 637 (2001); N.D. Tidwell, P.W. Eastwick & E.J. Finkel, ‘Perceived, Not Actual, Similarity Predicts Initial Attraction in a Live Romantic Context: Evidence from the Speed-dating Paradigm’, 20(2) Personal Relationships 199 (2013); Turban & Jones, above n. 14. This was thought to be the case because in order for similarity biases to manifest, an observer must first actually consider another person to be similar.48x Byrne, above n. 8.

The perceived similarity scale (Cronbach’s α = .8449x In statistics, Cronbach’s alpha is a measure used to assess the reliability, or internal consistency, of a set of scale or test items. See e.g.: https://data.library.virginia.edu/using-and-interpreting-cronbachs-alpha/.) consisted of the following three items: ‘I believe I have a similar character as the valuation professional, [Laura/Andrew] Matthews’; ‘I believe I have similar norms and values as the valuation professional, [Laura/Andrew] Matthews’; and ‘I believe that, in general, I am very similar to the valuation professional, [Laura/Andrew] Matthews.’ Participants were asked to indicate the extent to which they agreed with each statement on a 7-point Likert scale, ranging from ‘strongly disagree’ (1) to ‘strongly agree’ (7).Trustworthiness of the valuator. This variable was measured using three items (Cronbach’s α = .77), each representing one of the three dimensions of trustworthiness, ‘ability’, ‘benevolence’ and ‘integrity’, as put forward by Mayer et al.50x Mayer et al., above n. 23. The item measuring ability was: ‘I trust that the valuation professional, [Laura/Andrew] Matthews, is competent in the field of business valuation and is able to make a solid forecast for the purpose of this valuation.’ The item measuring benevolence was: ‘I trust that the valuation professional, [Laura/Andrew] Matthews, has an eye for the issues that are important in this case and that [she/he] will do [her/his] utmost best to meet me in my objectives.’ The item measuring integrity was: ‘I trust that the valuation professional, [Laura/Andrew] Matthews, is a person of integrity and will be fair to me in [her/his] considerations towards the value of the assets.’ Participants again responded on a 7-point Likert scale, ranging from ‘strongly disagree’ (1) to ‘strongly agree’ (7).

Trust in the valuation. We measured participants’ trust in the valuation outcome using four items (Cronbach’s α = .67). Considering the importance of risk-taking in trusting behaviour, we aimed to measure participants’ trust in the valuation outcome by including questions asking participants how likely they believed it was that they would perform certain actions involving risk based on the valuation outcome.51x R.C. Mayer and J.H. Davis, ‘The Effect of the Performance Appraisal System on Trust for Management: A Field Quasi-experiment’, 84(1) Journal of Applied Psychology 123 (1999). Specifically, we asked participants (1) ‘How likely do you consider it to be that you would accept the valuation outcome and start negotiating with the PE-firm based on [Laura/Andrew] Matthews’s valuation of GBP 18 million?’ and (2) ‘How likely is it that you would consult a second valuator to check the valuation outcome as determined by [Laura/Andrew] Matthews, realising there are additional costs to a second opinion that will affect the estate?’ Participants answered on a 7-point Likert scale ranging from ‘very unlikely’ (1) to ‘very likely’ (7). The other two items of the scale were (3) ‘I trust that the valuation outcome is representative of the market value of the assets’ and (4) ‘To what extent do you believe it is justified to try to determine a higher valuation outcome by arguing the outcome with the valuator, [Laura/Andrew] Matthews?’ Participants answered these last two questions on a 7-point Likert scale with the first ranging from ‘strongly disagree’ (1) to ‘strongly agree’ (7), and the second from ‘very justified’ (1) to ‘very unjustified’ (7).52x Since the internal consistency of the scale was below the benchmark range of .70 to .80 (C.E. Lance, M.M. Butts and L.C. Michels. The sources of four commonly reported cutoff criteria: What did they really say?. Organizational research methods, 9(2), 202-220, (2006)), we conducted exploratory factor analysis (EFA) to see if the four items do appear to measure a single construct. The EFA identified one single factor, and all the four items loaded on the factor satisfactorily. Also, the observed Cronbach’s alpha can be considered sufficient for theory-testing purposes (J.C. Nunnally and I.H. Bernstein. Psychometric Theory (3rd ed.). McGraw Hill, New York (1994)). Hence, based on the face validity of the scale combined with the internal consistency and EFA, we believe it is safe to assume the four-item scale is a valid measure of participants’ trust in the valuation outcome.

3.4 Part 2 of the Case: Outcome Manipulation

After the questions concerning perceived similarity, trustworthiness of the valuator, and trust in the valuation, participants were presented with either a positive outcome or a negative outcome to the case, depending on the experimental condition. The following case continuation scenario was presented to the participants.

3.4.1 Case (continuation)

Positive deal:

You moved forward with the PE-firm and started the negotiations based on the GBP 18 million valuation. The buyer probably made his own calculations as they were reluctant to accept the value of GBP 18 million. The Company’s creditors and other stakeholders were surprised by how long the deal took to close, knowing that private equity normally is keen to jump on a good opportunity. During the negotiation process, you were approached by a few other interested parties who ended their interest after hearing the negotiation price was GBP 18 million. Nonetheless, in the end the deal was closed for GBP 18 million. The Company’s creditors and other stakeholders felt that the deal was a good one and that a higher price for the assets was unattainable. They reported feeling satisfied, believing that a deal to cover the whole deficit of the estate was not feasible.

Negative deal:

You moved forward with the PE-firm and started the negotiations based on the GBP 18 million valuation. The buyer probably made his own calculations as they accepted the value of GBP 18 million instantly. The Company’s creditors and other stakeholders were surprised by how fast the deal was closed, knowing that private equity normally takes the time to negotiate. Additionally, after closing this deal, you were approached by a few other interested parties who indicated a value of GBP 25 million and above. Based on these factors, the Company’s creditors and other stakeholders felt that the deal was not a good one and that a higher price for the assets was attainable. They reported feeling frustrated, believing that a good enough deal to cover the whole deficit of the estate was feasible.

3.4.2 Notes on the Outcome Manipulation

With the positive-outcome scenario, we aimed to describe a situation in which negotiations with the PE-firm went very slow and difficult and that other parties refrained from making a bid when they learned the assets were valued at GBP 18 million. However, eventually the deal was closed at GBP 18 million and the creditors felt satisfied, believing this deal was the best they could have gotten out of the situation. In the negative-outcome scenario, we sought to describe that the PE-firm accepted the GBP 18 million offer instantly and that the trustee was later approached by other parties who indicated they were willing to pay GBP 25 million and above for the assets. Because of this, the creditors reported feeling frustrated as they believed a good enough deal to cover the entire deficit of the estate had in fact been feasible. Hence, the difference between the two outcome scenarios was the ease with which the deal was closed and the creditors and major stakeholders’ reactions to the deal (i.e. either happy or frustrated).

Please note that the outcome of the deal and the parties’ reactions need not reflect the quality of the valuation. Rather, the outcome of the deal may well be the result of the negotiation skills (good or bad) of the parties involved or the market sentiments surrounding the deal. The fair value of a company as determined by a valuator may very well diverge from the price that market participants ultimately pay for that company.3.4.3 Measures

Evaluation of the valuator’s role. We measured participants’ evaluation of the valuator using four items. First, participants were asked: ‘To what extent do you consider the valuation professional, [Laura/Andrew] Matthews, to be blameworthy or praiseworthy for the end result of the case (i.e. closing the deal at GBP 18 million)?’ – this was to be answered on a 7-point Likert scale ranging from ‘very blameworthy’ (1) to ‘very praiseworthy’ (7). Second, participants were asked to indicate to which extent they agreed or disagreed, on a 7-point Likert scale ranging from ‘strongly disagree’ (1) to ‘strongly agree’ (7), with the following three statements: ‘I believe that the valuation professional, [Laura/Andrew] Matthews, did [her/his] utmost best to determine a value according to the best of [her/his] knowledge and belief’; ‘Considering the outcome of the deal, I believe I would hire the valuation professional, [Laura/Andrew] Matthews, next time again’; ‘I believe that the end result of the case (i.e. closing the deal at GBP 18 million) is due to the work of the valuation professional, [Laura/Andrew] Matthews.’

The internal consistency (Cronbach’s alpha) of these four items was .56. This low score was due to the last item, perhaps because the part stating ‘…is due to the work…’ can be interpreted in multiple ways (e.g. causal responsibility, moral responsibility), and it might have been unclear to participants what was exactly meant. We therefore excluded this item from the scale, and the internal consistency of the remaining three items was .73 (i.e. acceptable).3.5 Analytical Approach

We used SPSS to test the hypotheses proposed in the study. Hayes’ PROCESS was used to test for (moderated) mediation in hypothesis 1. This macro applies bootstrapping and is widely used for conditional process analysis. As a nonparametric test, it has an advantage to the Sobel’s test in Baron and Kenny’s approach, in particular an increase in power. In addition, ANOVAs were used to test for the moderation in Hypotheses 2 and 3. Post hoc analysis was carried out to explore for moderation (i.e. MANOVA, ANOVA) and mediation (i.e. PROCESS) in hypothesis 3. Manipulation checks were done with independent samples t-tests.53x A.F. Hayes, Introduction to Mediation, Moderation, and Conditional Process Analysis. A Regression-based Approach (2013). R.M. Baron and D.A. Kenny, ‘The Moderator-Mediator Variable Distinction in Social Psychological Research: Conceptual, Strategic, and Statistical Considerations’, 51(6) Journal of Personality and Social Psychology 1173 (1986).

-

4 Results

4.1 Data Preparation

Considering the importance of reading the case and the details regarding the valuator properly, we determined a priori the exclusion criterion of having to spend at least 60 seconds reading the case. Even though this is a relatively arbitrarily chosen number, we do consider it to be a very lenient cut-off criterion, given that it would require a reading speed of 16.8 standard deviations (1 SD = 30 words/minute) above the average reading speed (M = 228 words/minute) in the English language to complete the case of 733 words within 60 seconds.54x S. Trauzettel-Klosinski and K. Dietz, ‘Standardized Assessment of Reading Performance: The New International Reading Speed Texts IReST’, 53(9) Investigative Ophthalmology & Visual Science 5452 (2012). For this reason, 11 participants (4%) were excluded from the analyses, resulting in a final sample of 261 participants. Importantly, excluding participants from further analyses did not affect any of the findings, as similar effect sizes and significance levels were found when the entire sample was analysed.

4.2 Similarity Bias

We tested the hypothesis that trust in a valuation can partly be explained by the similarity between the valuator and the insolvency professional judging the valuation and that this relationship is mediated by the perceived trustworthiness of the valuator. We first conducted a manipulation check to see whether the similarity manipulation affected the perceived similarity of the valuation professional. An independent samples t-test indicated that those in the high-similarity condition indeed perceived the valuator to be more similar to themselves (M = 4.07, SD = 1.05) than those in the low-similarity condition did (M = 3.56, SD = 1.07), t(259) = -3.84, p < .001, d = .48, suggesting the manipulation of similarity was successful.

Next, we used the Hayes’ PROCESS technique (10,000 bootstrap samples) to examine whether similarity (perceived and manipulated, in separate analyses) predicted the participants’ trust in the valuation and whether this relationship was mediated by the perceived trustworthiness of the valuator.55x A.F. Hayes (2013). Testing the effect of manipulated similarity, no significant relationship was found with the participants’ trust in the valuation.56x b =.11, SE = .13, 95% CI [-.16, .37]. However, when perceived similarity was used as the predictor variable, perceived similarity was found to predict trust in the valuation outcome, and this relationship was mediated by the perceived trustworthiness of the valuator, as indicated by a significant indirect effect.57x b =.12, SE = .03, 95% CI [.06, .18]. Hence, the hypotheses (H1a) that perceived similarity with the valuator predicts trust in a valuation and that this relationship (H1b) is mediated by the perceived trustworthiness of the valuator were supported. Table 1 shows further details of the mediation analysis.

We conducted a second mediation analysis in which the valuator’s firm profile (high profile vs. low profile) was included as a moderator variable for each of the mediation model’s paths. This was done to explore whether the relationships between perceived similarity, perceived trustworthiness, and trust in the valuation were dependent on the valuator firm’s profile. Results showed that none of the moderation effects were significant,58x All p-values > .46. suggesting that the observed relationships were robust and independent of the reputation of the valuator’s firm.Table 1 Unstandardised regression coefficients (b), standard errors (SE) and significance levels (p) for the proposed mediation model with perceived trustworthiness of the valuator (M) as the mediator of the relationship between perceived similarity (X) and trust in the valuation (Y).M (Trustworthiness) Y (Trust in Valuation) Antecedent b SE p b SE p X (Perceived similarity) .25 .05 < .001 .13 .06 .026 M (Trustworthiness) - - - .48 .07 < .001 Constant 4.14 .20 < .001 .88 .35 .013 R2 = .089 R2 = .214 F(1, 259) = 25.32, p < .001 F(2, 258) = 35.06, p < .001 4.3 Outcome Bias

We tested the hypothesis (H2) that participants’ evaluation of the role of the valuator in bringing about the outcome of the deal was affected by the outcome of that deal (i.e. positive vs. negative). We conducted an ANOVA with the deal-outcome condition (positive vs. negative) and the valuator’s firm profile (low profile vs. high profile) as the independent variables (including the interaction term), and the evaluation of the valuation professional’s role in bringing about the deal outcome as the dependent variable. Firm profile was included for exploratory purposes, to investigate whether any outcome effect might be more pronounced for either low-status firms or high-status firms. The ANOVA returned an insignificant interaction effect between outcome condition and firm profile, suggesting that the potential effect of outcome condition is independent of the status of the firm the valuator works for.59x F(1,257) = 0.80, p = .372, ηp2 = .003. Moreover, we did find a significant effect for the outcome condition,60x F(1,257) = 86.13, p < .001, ηp2 = .251. meaning that the participants judged the valuator more negatively following a negative deal outcome (M = 3.98, SD = 0.86) than after a positive deal outcome (M = 4.93, SD = 0.79), providing clear evidence for outcome bias in evaluations of valuators by insolvency practitioners. As such, hypothesis (H2) was supported.

4.4 Gender Bias

We explored whether the gender of the valuator explained variance in the perceived trustworthiness of the valuation expert and whether this effect depended on the gender of the insolvency professional. An ANOVA analysis with the perceived trustworthiness of the valuator as the dependent variable and the gender of the valuator and that of the participant as independent variables did not return a significant interaction effect between these two variables or any main effects.61x F(1,257) = 2.43, p = .12, ηp2 = .01.

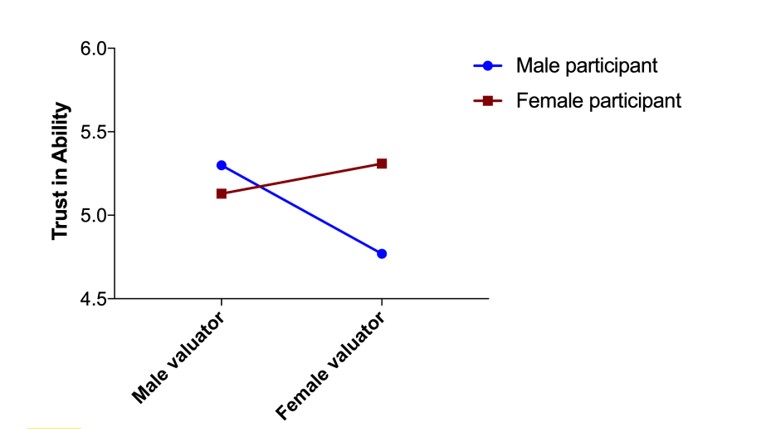

Yet, continuing the analyses a gender bias was revealed when we examined the three individual components of trustworthiness (i.e. ability, benevolence, integrity) separately. That is, the three items corresponding to the three dimensions of trustworthiness were subjected to a MANOVA with both the gender of the participant and the valuator as independent variables. The results showed a significant effect for the interaction between the two gender variables,62x F(3,255) = 2.70, p = .046, ηp2 = .03. but not for the main effects. Subsequent univariate analyses indicated that there was only a significant interaction effect for the item measuring trust in the valuator’s ability.63x F(1,257) = 6.53, p = .011, ηp2 = .03. Simple main effect analyses showed that male participants had more trust in the valuator’s ability when the valuator was also male (M = 5.30, SD = 1.05) than when the valuator was female (M = 4.77, SD = 1.10).64x F(1,138) = 8.52, p = .004, ηp2 = .06. Female participants on the other hand showed no difference in their judgments of the valuator’s ability based on the valuator’s gender, as their perception of the male valuator’s ability (M = 5.13, SD = 1.22) was not statistically different (F < 1) from their perception of the female valuator’s ability (M = 5.31, SD = 1.13). This interaction effect can be observed in Figure 1 where the blue line (with dots at the ends) shows that male participants have less trust in female valuators and the red line (with little squares at the ends) shows that female participants have marginally (but statistically not significant) more trust in female valuators.Mean scores on the measurement of trust in the ability of the valuator, separated for male and female valuators and male and female participants.

To explore whether this gender bias affected trust in the valuation through its effect on trust in the valuator’s ability, a mediation analysis was carried out. Indeed, the heightened trust in the valuator’s ability, when both the participant and the valuator were male, mediated the relationship between the gender of the valuator and the participant’s trust in the valuation, as indicated by a significant moderated mediation effect.65x Index = .29, 95% CI [.06, .54]. That is, the gender of the valuator predicted the participants’ trust in the ability of the valuator, and this subsequently predicted the trust in the valuation, but only if the participant was male, as indicated by a significant indirect effect for this group,66x b = -.21, SE = .08, 95% CI [-.37, -.06]. and the fact that such a mediation effect did not exist for female participants.67x b =.07, SE = .09, 95% CI [-.09, .25].

-

5 Discussion

In this experimental study, we explore the extent to which insolvency practitioners can be affected by similarity, outcome and gender biases when they evaluate valuators and their valuations. We find that if valuators are perceived by insolvency practitioners as more similar to themselves, they also perceive the valuators as more trustworthy and, in turn, have more trust in their valuations. Perceived similarity thus partly influences the insolvency practitioner’s trust in the valuation indirectly through its effect on the trustworthiness of the valuator. We also find that when insolvency practitioners evaluate valuators after they use their valuation reports for the sale of a company’s assets, the outcome of the deal affects the insolvency practitioners’ opinion of the valuators. In case of a good deal, valuators are perceived in a more positive light, whereas the same valuators are perceived more negatively after a bad deal. This outcome bias is independent of the status of the firm of the valuators (i.e. low status vs. high status). Finally, analyses reveal that male insolvency practitioners have more trust in the abilities of valuators when these valuators are also male. This increased trust in valuators’ abilities subsequently predicts an increased trust in the valuations. The women in this study did not demonstrate such gender bias.

Combined, these findings provide clear evidence for the existence of similarity bias and outcome bias among insolvency practitioners when dealing with business valuation issues and suggests that male insolvency practitioners appear to be affected by gender bias as well. In general, it shows that insolvency practitioners are prone to biases, just like other humans, while performing their duties – hence our somewhat provocative title: are insolvency practitioners human?68x We were inspired by an article of Helm, Wistrich and Rachlinski in the Journal of Empirical Legal Studies titled: ‘Are Arbitrators Human?’ (2016), hence the title of this article. Indeed, they are. -

5.1 Theoretical and Practical Implications

Our research shows that insolvency practitioners can be influenced by extra-legal factors when evaluating valuators and their valuations. The study thereby contributes to the literature by demonstrating that similarity, outcome and gender biases can manifest themselves in the insolvency context.

Specifically, we find empirical support for the notion that insolvency practitioners can be susceptible to similarity bias when dealing with complex valuation matters, thereby building on the previously discussed research on similarity biases in legal decision-making.69x E.g., Epstein et al., above n. 20; Gardner et al., above n. 19; Miller et al., above n. 18; Rector and Bagby, above n. 17. Moreover, empirical support is found for the notion that when insolvency practitioners have to evaluate valuators, they can be affected by outcome knowledge in such a way that a bad deal outcome causes them to perceive the valuator more negatively. This finding is in line with research on outcome bias in the legal context.70x E.g., Anderson et al., above n. 33; Harley, above n. 3; Kamin and Rachlinski, above n. 32; Kneer and Bourgeois-Gironde, above n. 33.

Importantly, empirical support is found for gender bias among male insolvency practitioners in such a way that male participants have more trust in the valuator’s ability when the valuator is also male compared to when the valuator is female. This is in line with studies showing gender bias in a legal context, specifically those studies demonstrating that men favour other men.71x Hodgson and Pryor, above n. 35; Resnik, above n. 35; Yourstone et al., above n. 35., 72x E.g., Fay and Williams, above n. 35; Macnell et al., above n. 35; Marlowe et al., above n. 35; Moss-Racusin et al., above n. 35. Our findings are also in line with studies that demonstrate that men typically have more trust in other men’s expertise and generally consider men to be more knowledgeable and skilful than women.73x E.g., Heilman and Haynes, above n. 36; Swim, above n. 36; Thomas-Hunt and Phillips, above n. 36. However, our finding is also in contrast with research showing that women are harsher when judging men.74x Johansson et al., above n. 37.

Equally important are the practical implications of our study. In business, the interests of stakeholders are frequently not aligned. Consequently, there are many disputes between stakeholders involving, or even focusing on, a valuation. In their capacity as representatives of stakeholders’ interests, or as independent experts representing the court, insolvency practitioners are confronted with valuation reports and valuation issues, and they must form opinions about the valuation and the valuator. In an ideal world, the evaluation of valuators and valuations is solely based on the quality of the valuation and the correctness of the applied valuation framework. Following our premise that it is unlikely that insolvency practitioners are able to judge valuations on their own merit, we indeed find that other extra-legal factors influence insolvency practitioners’ perception about valuations and valuators.

The implication of this is that, regardless of whether a valuation is demonstrably correct and complies to all (theory-based) valuation standards and requirements and is free from valuation input biases, both the valuation and the valuator can be judged as inadequate and vice versa. This can be problematic, as from a pragmatic standpoint it can obscure the efficient settlement of valuation disputes. From a more principle-oriented standpoint, it could be argued that valuators might be unduly blamed, discredited and/or distrusted despite having delivered sound work, violating a fair treatment in legal proceedings. Indeed, disputes about or involving valuations might be conducted on improper grounds and even be unnecessarily extended, which is not beneficial for any stakeholder. Also, biases may lead to improper judgments regarding questions related to (but not limited to) the following: perceived chances of survival and with that the alleged viability of a distressed company, perceived (mis)behaviour of company directors of a bankrupt firm, or the likelihood of a multi-creditor workout deal. In addition, if it is indeed the case that men have less trust in the expertise of female practitioners, this is clearly problematic, particularly in male-dominated industries, such as law firms in general and the judiciary specifically.

Importantly, neither worldwide valuation practice nor legal practice currently offers clear answers to counter these problems, mainly because cognitive biases are difficult to neutralise or eliminate. Both valuation practitioners and insolvency practitioners must be more aware of the effects of biases, as these can enlarge the magnitude of a conflict or ignite new conflicts. We therefore emphasise the importance of developing new approaches and methods to reduce the impact of biases in the insolvency industry. Following its expertise in drafting codes of conduct, like for instance the “Statement of Principles for a Global Approach to Multi-Creditor Workouts”, INSOL International could take the lead in promoting such “debiasing strategies”. This could include fostering further research on the topic, as well as developing specific training programmes to raise awareness for the topic and to discuss potential solutions.

Our experience informs us that biases may lead to strong opinions, controversy and heated debates in the society, especially on the topic of gender bias. We are also aware of the fact that diversity and inclusion (D&I), psychological safety as well as gender gaps regarding compensation are important problems in the professional services industry worldwide. We hope that this study also helps law and accountancy firms to pick up the gauntlet in this respect. -

5.2 Limitations and Future Research

Our findings are based on an ecologically valid sample with realistic study materials that included a real-world business case as well as a summary of a valuation report. Taken together, these factors benefit the external validity and overall generalisability of our study. We nonetheless acknowledge limitations. An arguable weakness of the study is the compressed manner in which the financial and valuation assumptions were presented. Although participants gave positive feedback on the presented case, we acknowledge that it is difficult to establish with certainty that our findings are fully generalisable to real-life cases. For reasons of brevity, participants were not presented with a complete valuation report. Hence, it might be that different results emerge when a detailed valuation report is presented. However, we consider this to be unlikely as we suspect that many insolvency practitioners are not trained to analyse and fully grasp a complete valuation report and that they generally do not have the time to do so.

We presented a case that concerned an insolvent company whose assets were sold to simulate a ‘going-concern’ situation. Therefore, it remains an open question whether the findings presented in this article can be generalised to different cases outside the context of restructuring and insolvency, which might be dealt with by legal practitioners other than the restructuring and insolvency specialists used in this study. However, given that cognitive biases are largely universal, we suspect that legal practitioners with a different legal focus will be similarly affected. Nonetheless, future research could investigate the generalisability of the present findings across legal contexts.

In addition, participants were not incentivised (i.e. did not receive monetary compensation for their participation), and this may have affected the response rate as well as participants’ motivation to carefully process and respond to the survey. However, given that insolvency lawyers earn significant fees in their professional work, we expected that a small financial incentive would not have increased their motivation much. Instead, we relied on their intrinsic motivation and commitment to advancing their professional field. Furthermore, we applied detection methods – an a priori exclusion criterion, an attention check item and an ex ante manipulation check – to increase data quality and exert a motivational influence.75x See also H. Shamon and C. Berning, ‘Attention Check Items and Instructions in Online Surveys with Incentivized and Non-Incentivized Samples: Boon or Bane for Data Quality?’, 14(1) Survey Research Methods 55 (2020).

The order in which some measures to test hypothesis 1 were presented is also a factor to be considered. We chose to present the measures in the order consistent with the proposed mediation model (i.e. perceived similarity – trustworthiness of the valuator – trust in the valuation). Participants’ perceived similarity with the valuator was therefore measured before perceived trustworthiness of the valuator and before trust in the valuation. This order may have increased participants’ awareness of their similarity with the valuator and affected their answers to the subsequent measures. However, presenting the measures in a different order raises the same concern. For example, it could be that when the trust in the valuation measure was presented first, it would subsequently have affected the answers on the other two measures. A participant indicating a high trust in the valuation may, for example, be motivated to subsequently indicate high levels of perceived similarity. We therefore acknowledge the possibility of ‘order effects’ having an influence on the results of the study and would encourage future research to examine this potential effect by presenting the similarity measure after the dependent variable.